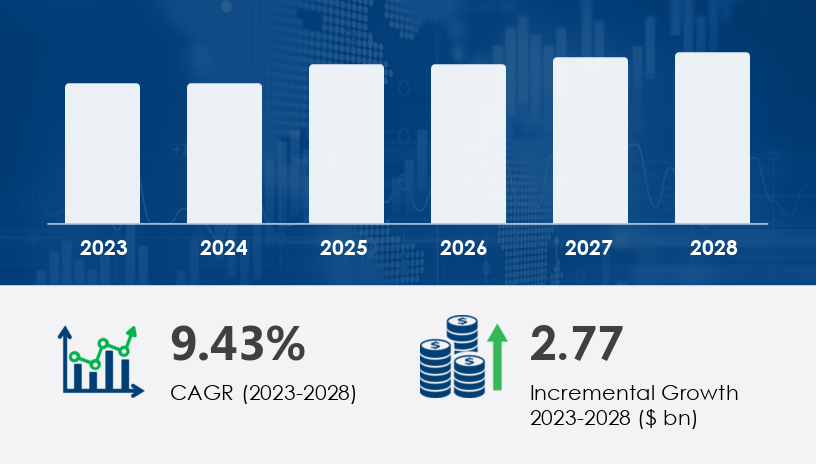

The sulfur recovery technology market size is on track to increase by USD 2.77 billion between 2024 and 2028, growing at a CAGR of 9.43%. This surge is powered by tightening global emission norms and the rising need for cleaner fuels across industrial sectors. This forecast provides strategic guidance for stakeholders in oil and gas, petrochemicals, and energy sectors, alongside a free report sample to help businesses understand market dynamics and optimize their compliance and growth strategies.

Explore trends, segmentation, and growth drivers: View Free Sample PDF

The sulfur recovery technology market encompasses various processes and technologies aimed at extracting sulfur from industrial waste gases, primarily hydrogen sulfide (H₂S). This is crucial for industries such as oil and gas, where sulfur compounds are prevalent. The market's growth is fueled by the need to comply with environmental regulations and the increasing demand for sulfur in various applications

Sulfur recovery involves converting hydrogen sulfide (H₂S) into elemental sulfur using chemical and thermal processes. This is especially vital in:

Oil refineries

Natural gas processing facilities

Power plants

Petrochemical plants

Sulfur is later used in fertilizers, cosmetics, pharmaceuticals, and food packaging.

The global sulfur recovery market is competitive and innovation-driven. Major players are investing in advanced technologies and global expansion.

These companies focus on strategic collaborations, cost-effective technology development, and sustainable emissions reduction solutions.

Request Your Free Report Sample – Uncover Key Trends & Opportunities Today!

Claus Process: Most widely adopted; dominates market share.

Tail Gas Treatment: Gaining momentum due to high recovery efficiency.

Others: Including direct oxidation and advanced catalytic systems.

Oil & Gas: Core driver due to refining operations.

Chemical Processing: Uses sulfur for intermediate production.

Power Generation: Focus on clean energy compliance.

Metal Processing: Controls emissions during smelting.

APAC (45% share): Led by China and India, with shale gas projects and expanding refinery capacities.

North America: Mature market, driven by Clean Air Act and refinery upgrades.

Europe: Focus on EU Industrial Emissions Directive compliance.

Middle East & Africa: Investments in upstream oil & gas.

South America: Emerging interest, especially in Brazil.

Stricter global emission regulations, such as the EU’s Industrial Emissions Directive and the U.S. Clean Air Act, are pressuring industries to implement advanced sulfur recovery systems.

Rapid urbanization and industrial growth in China and India have made APAC the fastest-growing region. For instance:

China’s Sichuan basin shale gas development boosts SRU demand.

Indian Oil’s Koyali refinery modernization (LuPech project) reflects local capacity growth.

Refineries worldwide are upgrading or installing SRUs (Sulfur Recovery Units) to meet regulatory norms. This is particularly visible in:

Maritime fuel production

Power plants switching to low-sulfur fuels

Petrochemical complexes expanding polypropylene production

45% of global market growth between 2024–2028.

Investments in refining capacity and petrochemical plants.

High sulfur content fuels drive need for SRUs.

High compliance with environmental standards.

Refineries incorporate tail gas treatment to meet EPA standards.

EU policies encourage low-emission technologies.

Refiners focus on emission reduction and energy efficiency.

The cost of setting up a sulfur recovery unit can reach tens of millions of dollars. This includes:

Claus reactors

Amine treating systems

Tail gas treatment units

Specialized catalysts and corrosion-resistant materials

Heat recovery systems and process optimization required.

Maintenance and catalyst replacement costs add to lifecycle expenses.

The sulfur recovery market plays a critical role in ensuring environmental compliance and meeting stringent emission standards across key industries such as oil refining, petrochemical plants, and natural gas processing. Central to this market is the Claus process, a widely used technology for sulfur extraction from sour gas streams, particularly in refinery processes and gas processing facilities. The Claus unit—often integrated with tail gas treatment systems—enables the conversion of hydrogen sulfide (H₂S) into elemental sulfur, a valuable byproduct used in fertilizer production and chemical manufacturing. Supporting components such as sulfur condensers, catalytic reactors, and reheat exchangers ensure high sulfur recovery efficiency. The market is driven by global concerns over air pollution and acid rain, prompting refinery upgrades for enhanced desulfurization and sulfur management. In addition to traditional methods like amine treating, emerging techniques such as biodesulfurization are gaining attention, complementing flue gas desulfurization systems to reduce sulfur emissions and promote cleaner fuels.

Request Sample of our comprehensive report now to stay ahead in the market

The sulfur recovery technology market is expected to witness significant growth through 2029, driven by environmental regulations and the global emphasis on sustainable industrial practices. Technological innovations, such as advanced catalysts and integration with digital monitoring systems, will play a crucial role in shaping the market's future.

Expert Prediction: "The market's trajectory will be defined by the industry's ability to adapt to regulatory pressures and technological advancements," predicts a Technavio analyst.

Are industry players prepared to embrace innovation and meet the evolving demands of sulfur recovery?

For Claus Process Operators:

Invest in research and development to enhance catalyst performance.

Implement real-time monitoring systems to optimize process efficiency.

Collaborate with technology providers for continuous process improvements.

For Tail Gas Treatment Units:

Explore cost-effective solutions to manage operational expenses.

Train personnel in handling complex treatment processes.

Adopt modular designs for scalability and flexibility.

For Oil and Gas Recovery Sources:

Customize recovery technologies to handle specific feedstock characteristics.

Monitor market trends to anticipate shifts in feedstock availability.

Engage in strategic partnerships to access emerging markets.

Request Sample of our comprehensive report now to stay ahead in the market

The sulfur recovery market is shaped by a combination of technical advancements, regulatory pressures, and industrial demands across industrial processes. Claus technology remains the cornerstone of sulfur recovery units, supported by innovations in tail gas treatment for improved emission control. The growing need for environmental regulations compliance, especially in managing sulfur compounds within sour crude oil and gas streams, has driven investments in sulfur management infrastructure. The market also sees rising integration with petroleum refining operations and chemical manufacturing facilities, where sulfuric acid and other sulfur byproducts are critical inputs. As H2S removal technologies advance, operators are focusing on optimizing sulfur recovery efficiency while minimizing operational costs. These trends underscore the importance of sulfur condensers, catalytic reactors, and reheat exchangers in maximizing recovery rates. The market’s future is also shaped by the increasing adoption of cleaner fuels, the expansion of biodesulfurization techniques, and the growing demand for effective solutions in flue gas desulfurization, all contributing to a more sustainable and regulated sulfur recovery landscape

As we move toward a carbon-conscious future, sulfur recovery technology has become more than just a regulatory checkbox—it’s a strategic imperative. From the burgeoning refineries of Asia to the sustainability-focused plants of Europe and North America, the market is evolving rapidly.With increasing pressure from global emissions standards, companies that proactively invest in sulfur recovery will not only ensure compliance but gain a competitive edge in the cleaner energy economy.

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.