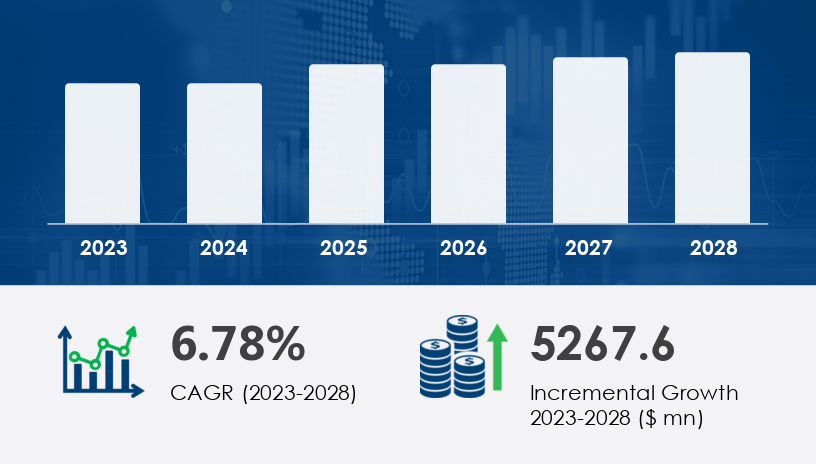

The global echocardiography (ECG) devices market is poised to expand by USD 5.27 billion from 2023 to 2028, registering a compound annual growth rate (CAGR) of 6.78%. This growth reflects a pivotal shift in how cardiac diagnostics are evolving—, where technology integration and cardiovascular disease prevalence are driving demand.For more details about the industry, get the PDF sample report for free

At the heart of this market expansion lies the increasing incidence of cardiac disorders, including heart valve disease, coronary heart disease, atrial fibrillation, and heart failure. Cardiovascular disease remains a global health crisis, with over 92 million adults affected and approximately 20.5 million deaths attributed to uncontrolled hypertension in 2021.

Echocardiography, as a non-invasive diagnostic technique, plays an indispensable role by using ultrasonic sound waves to image heart chambers, valves, and detect blood clots. This capability ensures that heart-related conditions can be diagnosed early, improving patient prognosis and reducing long-term healthcare costs.

A defining trend in the echocardiography landscape is the integration of advanced technologies. Innovations such as AI-driven auto-measure applications, neural network-based algorithms, and 2D echo imaging are revolutionizing how physicians assess cardiac function. Institutions like the Heart Center Leipzig are pioneering these advancements with devices like the Ultrasound 3300, emphasizing measurement accuracy and workflow optimization.

Additionally, the market is witnessing the rise of portable and wireless ECG systems, which expand diagnostic access beyond traditional clinical settings. The combination of stress echocardiography and Doppler imaging further enhances the diagnostic value by evaluating heart performance during physical exertion.

Despite technological leaps, high costs of ECG products and procedures remain a persistent hurdle. Healthcare providers, particularly smaller hospitals and diagnostic centers, often face budgetary constraints exacerbated by regulatory pressures and rising operational expenses. This financial strain has prompted some facilities to opt for traditional ECG alternatives over state-of-the-art echocardiography systems.

However, the continued push for early, noninvasive diagnosis and telemedicine adoption is helping mitigate these challenges by improving accessibility and reducing hospital stay durations.

The hospitals segment holds a dominant position in the market and is projected to see significant growth through 2028. In 2018, hospitals accounted for USD 7.34 billion in value and have shown steady gains since.

Hospitals utilize transthoracic and transesophageal echocardiography to diagnose complex heart conditions such as hypertrophic and dilated cardiomyopathies. These methods offer high diagnostic accuracy with no known adverse effects, making them integral to emergency and routine cardiac care. The limited availability of echocardiography in all hospital settings has also spurred diagnostic centers to adopt these devices and cater to unmet patient needs.

The market is divided into three primary product segments:

Resting ECG Devices

Ambulatory ECG Devices

Stress ECG Devices

Stress echocardiography continues to gain traction due to its ability to assess heart function under load, proving vital in diagnosing coronary heart disease and heart failure. Meanwhile, ambulatory devices enable continuous cardiac monitoring, supporting telemedicine frameworks and remote diagnostics.

The North American region is expected to contribute 45% to global market growth, with the U.S. and Canada leading the charge. The high prevalence of cardiovascular diseases, coupled with a growing geriatric population—which made up 17.3% of the U.S. population in 2022, according to the U.S. Census Bureau—drives frequent demand for echocardiography procedures.

Additionally, government and nonprofit-led initiatives aimed at early detection and prevention of cardiovascular disease have catalyzed adoption. The region also boasts strong infrastructure for AI-enabled devices and remote monitoring solutions, fostering widespread use of transthoracic and transesophageal methods.

In Germany, high healthcare expenditure and strong R&D frameworks support market growth. Hospitals and academic institutions continue to adopt advanced echocardiography solutions, integrating them into patient pathways for better outcomes.

Countries such as China and Japan are emerging as key markets, driven by a rising elderly population and growing public awareness around cardiovascular health. The expansion of healthcare access in these nations is also fueling equipment demand.

The rest of the global market sees slower growth but remains significant. As developing nations enhance their healthcare infrastructure, particularly around noninvasive diagnostics, echocardiography device penetration is expected to increase steadily.

Get more details by ordering the complete report

The Semiconductor Advanced Packaging Market is rapidly evolving, driven by the demand for high-performance, compact, and energy-efficient electronic systems. Technologies like flip chip, fan-out WLP, 2.5D packaging, and 3D ICs are becoming central to next-generation chip designs. Applications such as CMOS image sensors, MEMS sensors, logic devices, and memory devices are adopting these advanced packaging methods to enhance processing capabilities and reduce form factors. The rise in wireless connectivity needs is fueling innovations in system-in-package and chiplet integration solutions, with cutting-edge hybrid bonding techniques supporting more robust interconnectivity. Key processes like wafer bumping, die attach, and ball grid array mounting play crucial roles in manufacturing efficiency. Packaging solutions such as embedded die, high-density interconnects, and advanced substrates including organic substrates and leadframe packaging are essential for meeting modern design requirements. Additionally, materials such as encapsulation resins, bonding wire, and ceramic packages are vital for improving thermal management and durability across various end-user applications

The competitive landscape is marked by innovation-driven partnerships, mergers, and geographic expansions. Prominent players include:

General Electric Co.

Medtronic Plc

Koninklijke Philips N.V.

Clarius Mobile Health

Ultrasound Workspace

AliveCor Inc.

Baxter International Inc.

Bittium Corp.

SCHILLER AG

iRhythm Technologies Inc.

These companies are leveraging AI and cloud-based platforms to enhance device capabilities, reduce diagnostic turnaround time, and improve measurement consistency.

For more details about the industry, get the PDF sample report for free

Research reveals that advanced packaging technologies are critical for supporting high-performance applications in power devices, RFID chips, AI processors, and HPC chips, especially within the context of expanding 5G modules and IoT devices. The automotive sector is also benefiting from robust solutions for automotive ICs, reflecting the growing importance of miniaturized electronics in electric and autonomous vehicles. Innovations in heterogeneous integration, wafer-level packaging, and the development of thin wafers are enabling the rise of multi-chip modules with improved signal integrity and power efficiency. Additionally, the market is seeing an increased demand for compact ICs, high-frequency chips, and nano-sized chips, all of which are fundamental to space-constrained and high-speed applications. The synergy between chip packaging advancements and the broader innovation in integrated circuits and semiconductor dies highlights the strategic importance of packaging as not just a manufacturing step, but a performance enabler in modern semiconductor design.

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.

devices market 2024-2028")