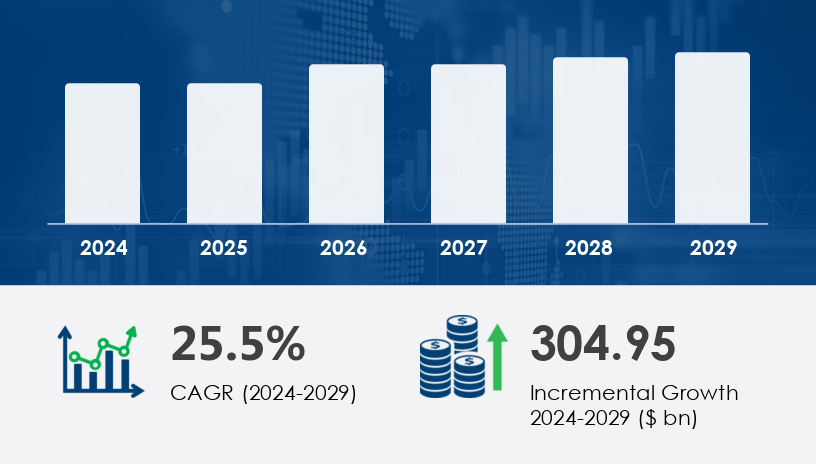

The digital payment market is poised for significant expansion, driven by increasing transaction volumes and the shift toward mobile-first commerce. In 2024, the global market stood at a robust valuation, with projections indicating an increase of USD 304.95 billion by 2029, growing at a compound annual growth rate (CAGR) of 25.5%. The industry is evolving in response to a surge in smartphone usage, digital wallets, blockchain adoption, and rising demand for seamless transactions across ecosystems.

Explore trends, segmentation, and growth drivers: View Free Sample PDF

A primary driver of the digital payment market is the rising number of online transactions, particularly enabled by smartphones and mobile wallets. Consumers prefer digital channels for their speed, security, and convenience over traditional methods. The popularity of digital wallets stems from features such as seamless registration, user-friendly dashboards, and fast merchant-consumer interactions. These wallets support in-store and online payments through NFC-enabled POS terminals, enabling real-time transactions that enhance both customer satisfaction and retailer marketing effectiveness. According to analysts, this growth is further catalyzed by the increasing penetration of smartphones and the readiness of retailers to integrate mobile payment systems into their operations.

One of the most notable trends reshaping the digital payment market is the growing emergence of mobile apps for shopping and financial transactions. Consumers are shifting from websites to mobile apps due to the ubiquity of smart devices and the superior convenience mobile apps offer. Particularly in high-growth markets like India, mobile payments are experiencing exponential adoption, a trend that accelerated during the pandemic. However, in developing economies with uneven internet access, app-only models pose challenges. Thus, digital payment providers must maintain platform flexibility—serving both mobile-first and multi-platform users—to broaden reach and maximize user engagement. This dual-channel strategy is essential for businesses looking to thrive in a mobile-driven world.

The digital payment market is experiencing rapid transformation driven by consumer demand for seamless, secure, and instant transactions. Central to this shift are tools like the digital wallet, mobile payment, and contactless payment, supported by robust payment gateways that ensure smooth transactions across platforms. Emerging trends such as blockchain payment and cryptocurrency transactions are revolutionizing the way value is exchanged online, while peer-to-peer payment systems and online banking solutions continue to dominate day-to-day digital transfers. The adoption of cardless payment and instant payment services, especially in high-velocity retail environments, is reshaping expectations. Innovative options like QR code payment, NFC payment, and partnerships with reliable payment processors are enabling widespread merchant adoption. Additionally, fintech platforms are enhancing e-commerce checkout systems with secure features like tokenization security and biometric authentication, while digital alternatives such as digital currency, payment APIs, and cross-border payments facilitate both local and global commerce.

The digital payment market is segmented into the following categories:

By End-user

Large enterprises

SMEs

By Component

Solutions

Services

By Deployment

On-premises

Cloud

By Method

Digital wallets

Bank cards

Digital currencies

By Application

BFSI

Media and entertainment

IT and telecommunication

Hospitality

Healthcare

Among the various end-user categories, large enterprises represent the leading segment, both in terms of market share and growth. Valued at USD 28.10 billion in 2019, this segment has demonstrated consistent expansion, driven by increasing transaction volumes in banking, IT, manufacturing, and hospitality sectors. These enterprises are early adopters of real-time payments, open banking APIs, and cryptocurrency options. Innovations such as biometric authentication, digital wallets, and QR code-based payments have become standard in their payment ecosystems. According to analysts, large enterprises prioritize payment security, speed, and integration, enabling them to deliver a superior customer experience and retain market leadership in a highly competitive environment.

Regions Covered:

North America

Europe

APAC

South America

Middle East and Africa

Rest of World (ROW)

Asia-Pacific (APAC) is projected to contribute a substantial 35% to the global market growth from 2025 to 2029, making it the top-performing region. This surge is largely driven by countries like India, China, South Korea, and Japan, where digital transformation and smartphone adoption are accelerating rapidly. Payment innovations such as QR code payments, mobile wallets, and peer-to-peer transfers are being rapidly adopted in both urban and rural markets. Additionally, companies in APAC are embracing subscription and instant payments, facilitated by robust open banking infrastructure and government-backed digital identity systems. Analysts attribute the region’s growth to the increasing collaboration between fintech startups and traditional financial institutions, enhancing accessibility, affordability, and inclusivity in digital financial services.

Request a Free Sample of our comprehensive report now

Despite rapid advancements, the digital payment market faces persistent challenges, with privacy and security concerns being the most significant. Digital payment platforms transmit sensitive personal and financial data, making them frequent targets for phishing attacks, hacking, and data breaches. Additionally, many service providers share user data with third parties for marketing, further undermining consumer trust. Criminals exploit these vulnerabilities by creating fake websites and sending phishing messages to obtain confidential information. These threats not only compromise data security but also hamper adoption, especially in markets with low digital literacy. According to market insights, addressing these concerns with robust security protocols, multi-factor authentication, and transparency is critical for sustained market growth.

Market research indicates growing investment in emerging payment infrastructures such as micropayment systems, smart contracts, and intelligent payment orchestration platforms, which streamline complex transaction flows. The rise of real-time payments, virtual cards, and mobile POS solutions are enhancing both consumer convenience and business flexibility. To reduce risk, technologies like payment tokens, fraud detection, and chargeback prevention are being integrated within systems offered by payment aggregators. Businesses are also adopting digital back-office tools including digital invoices, recurring payment models, and advanced payment encryption to support secure, scalable operations. Regulatory shifts have encouraged the growth of open banking and centralized payment hubs, supported by continuous transaction monitoring. Enhanced hardware and protocols such as the EMV chip, combined with real-time payment analytics, deliver insights for improved decision-making. Meanwhile, the integration of wallet apps, payment middleware, secure checkout, and full payment integration capabilities further empower businesses to support new models like Buy Now, Pay Later (BNPL). These systems are protected by strong payment authentication protocols and serve global needs through digital remittance services.

The digital payment ecosystem is becoming increasingly interconnected, automated, and intelligent. As global commerce accelerates, success will hinge on the seamless integration of secure, real-time technologies and user-friendly interfaces. Providers that invest in analytics, fraud prevention, and open infrastructure—while embracing emerging payment models and regulatory compliance—will lead the digital finance revolution.

The competitive landscape of the digital payment market is shaped by innovation and strategic collaboration. Key players such as ACI Worldwide Inc., PayPal Holdings Inc., Mastercard Inc., Visa Inc., and Stripe Inc. are deploying real-time payment overlays, biometric verification, and payment analytics platforms to strengthen their offerings. For instance, ACI Worldwide provides digital payment overlay services that enable instant settlements through real-time processing, increasing both speed and efficiency.

Fintech companies are also focusing on subscription-based payments, mobile money, and alternative payment methods to diversify their revenue streams and cater to niche markets. Meanwhile, payment aggregators are disrupting the status quo by offering API-integrated platforms that enhance cross-border capabilities and reduce payment friction.

Further, open banking frameworks, cloud deployments, and contactless payments are emerging as central pillars of digital payment strategies. Firms are also integrating AI and payment data analytics to refine fraud detection and boost conversion rates. These strategies are allowing businesses to offer a personalized and secure user experience, improving customer retention and operational efficiency.

The digital payment market is undergoing a period of robust growth, forecast to expand by USD 304.95 billion from 2025 to 2029 at a CAGR of 25.5%. Growth is being fueled by the widespread adoption of smartphones, digital wallets, and mobile apps, particularly among large enterprises and in APAC. While security and privacy challenges persist, continuous innovation and compliance-driven development are helping market players navigate these obstacles.

As the digital payment ecosystem becomes more interconnected and user-centric, opportunities will continue to emerge across sectors. Businesses that prioritize secure, seamless, and multi-channel payment experiences—backed by AI-driven analytics and strategic alliances—will be best positioned to lead in this rapidly evolving landscape.

1. Executive Summary

2. Market Landscape

3. Market Sizing

4. Historic Market Size

5. Five Forces Analysis

6. Market Segmentation

6.1 End-User

6.1.1 Large Enterprises

6.1.2 SMEs

6.2 Component

6.2.1 Solutions

6.2.2 Services

6.3 Deployment

6.3.1 On-Premises

6.3.2 Cloud

6.4 Method

6.4.1 Digital wallets

6.4.2 Bank Cards

6.4.3 Digital currencies

6.5 Application

6.5.1 BFSI

6.5.2 Media and entertainment

6.5.3 IT and telecommunication

6.5.4 Hospitality

6.5.5 Healthcare

6.6 Geography

6.6.1 North America

6.6.2 APAC

6.6.3 Europe

6.6.4 South America

6.6.5 Middle East And Africa

6.6.6 ROW

7. Customer Landscape

8. Geographic Landscape

9. Drivers, Challenges, and Trends

10. Company Landscape

11. Company Analysis

12. Appendix

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.