The Digital Education Content Market is being driven by Rapid penetration of Internet-enabled devices

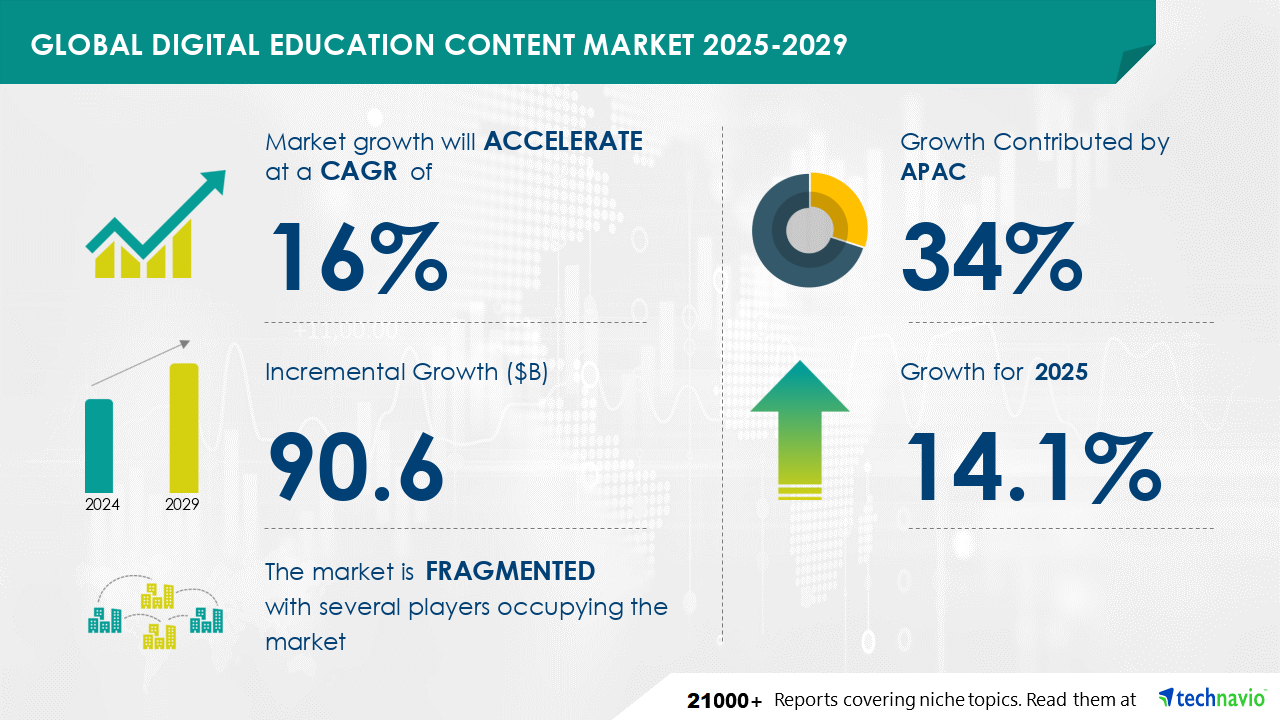

The Digital Education Content Market is expected to grow at a CAGR of 16% during 2024 and 2029. During this period, the market is also expected to show a growth of USD 90.6 billion. The digital education content market is witnessing a significant surge in new product launches from vendors, driven by the escalating demand for advanced and efficient learning solutions. This trend is fueled by the evolving requirements of learners and educators. In line with this trend, Coursera unveiled Clips on May 5, 2022, a new feature providing over 10,000 short videos and lessons from top global corporations and universities, aiming to expand to over 200,000 videos by year-end. This underscores the increasing investment in innovative digital education solutions.

Get more information on Digital Education Content Market by requesting a sample report

The market is segmented based on

According to Technavio, There are several factors that are causing the market to flourish during the forecast period, which are as follows:

However, the market also witnesses some limitations, which are as follows:

Rich Experience: 20+ years leading global market research, trusted insights across industries.

Unlock Business Potential with Technavio: Maximize ROI with Technavio's tailored market research: deep dives and actionable insights.

Your Guide to Market Success: Empower your business with Technavio's market research and future-proof your decisions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

204 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16% |

|

Market growth 2025-2029 |

USD 90.6 billion |

|

Market structure |

fragmentation |

|

YoY growth 2024-2025(%) |

14.1 |

|

Key countries |

US, China, Canada, UK, Germany, Brazil, India, France, Japan, and Saudi Arabia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Find out which segment is leading the market by accessing the free PDF report

In the realm of Digital Education, tools for creating courseware are essential. These include curriculum design software and authoring platforms. Digital literacy training is crucial for students and professionals. Online tutoring platforms and teacher training modules offer personalized feedback through skill mastery assessments and learning analytics reporting. Interactive whiteboards and virtual labs provide immersive learning experiences. Competency frameworks ensure effective knowledge transfer. E-portfolio management and collaborative learning spaces foster student engagement. Assessment automation tools and online exam proctoring ensure accurate measurement of learning outcomes. Learning object repositories and multimedia content offer accessibility. Data visualization techniques and personalized feedback systems enhance the learning experience. Educational simulations and virtual labs provide hands-on training. Knowledge transfer strategies and training effectiveness metrics ensure continuous improvement. Feedback mechanisms and assessment tools promote continuous learning.

The global market for interactive media and services encompasses businesses specializing in the creation or distribution of digital content via proprietary learning management systems, online course platforms, and interactive learning modules. This sector, often referred to as the digital advertising market, generates significant revenue through pay-per-click advertisements. The media and entertainment industry, which includes these companies, is projected to expand at a moderate rate. According to Technavio, the industry's size is determined by the consolidated revenue generated by organizations providing media, entertainment, and interactive media and services. Key players in this sector include search engines, social media and networking platforms, online classifieds, and educational review companies.. Industries are leveraging the products belonging to the market for customer engagement, transactional notifications, and promotional offers.

Technavio Research

Jesse Maida

Media & Marketing Executive

US: +1 844 364 1100

UK: +44 203 893 3200

Email: media@technavio.com

Website: www.technavio.com/

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.