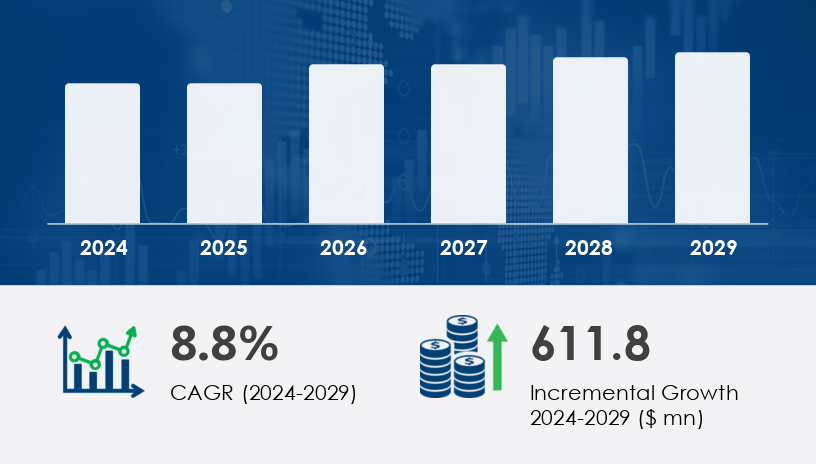

The Blood-Grouping Reagents Market is projected to grow by USD 611.8 million between 2025 and 2029, expanding at a CAGR of 8.8%. This surge is primarily fueled by the increasing global prevalence of chronic disorders such as cancer and cardiovascular diseases, both of which frequently necessitate blood transfusions. In this context, blood-grouping reagents are indispensable tools, ensuring compatibility between donor and recipient blood and mitigating risks like transfusion reactions and hemolysis.Healthcare systems are investing in innovative technologies that streamline diagnostic processes. Automated blood grouping systems and point-of-care diagnostic devices are reshaping the operational landscape of hospitals and labs, ensuring accuracy and reducing turnaround times. These advancements, coupled with the growing demand for transfusion safety, are expected to accelerate adoption across healthcare infrastructure.For more details about the industry, get the PDF sample report for free

The blood-grouping reagents market is categorized by end-users, techniques, and product types, each contributing to the sector’s overall momentum.

Hospitals and Blood Banks (Largest Segment)

Clinical Laboratories

Academic and Research Institutes

Among these, hospitals and blood banks dominate the market, driven by rising hospital admissions related to chronic conditions, emergency interventions, and trauma. In 2019, this segment alone accounted for USD 424.40 million and has continued to show robust growth.

PCR-based and Microarray Techniques

Assay-based Techniques

Massively Parallel Sequencing Techniques

Serology

Technologies such as molecular typing and HLA typing are being widely adopted, especially for advanced diagnostics and transplantation procedures. These techniques allow high-accuracy detection of ABO and Rh antigens, minimizing mismatches and enhancing transfusion safety.

Anti-sera Reagents

Red Blood Cell Reagents

Blood Bank Saline

Others

Each of these plays a role in blood typing, cross-matching, and antibody screening, making them indispensable to patient care in critical and surgical environments.

The North American region is expected to contribute 49% to the global market growth between 2025 and 2029. This expansion is particularly evident in the United States, where a growing elderly population and rising incidences of chronic illnesses are driving demand. According to the National Program of Cancer Registries (NPCR), over 29 million invasive cancer cases have been diagnosed in the US since 2003, highlighting the urgent need for reliable blood grouping and compatibility testing.

Get more details by ordering the complete report

The increasing prevalence of chronic disorders, especially in aging populations, is the primary market driver. In 2023 alone, the US saw 1.96 million new cancer cases, many requiring multiple transfusions during treatment. Additionally, chronic conditions like diabetes and cardiovascular diseases, which are leading causes of death in the US, further necessitate reliable blood-grouping solutions in emergency departments and intensive care units.

These reagents are critical for determining Rh factor and HLA types, ensuring safe transfusions and organ transplants. Moreover, innovations like automated systems, rapid test kits, and integration of AI and machine learning in diagnostics are significantly reducing turnaround times while improving accuracy and operational efficiency.

One of the most influential trends is the technological advancement in diagnostic devices. Traditional serological methods are being replaced with molecular typing, capable of identifying gene-level mutations and polymorphisms associated with blood-group antigens. This advancement leads to more precise identification and prediction of antigens, thus minimizing risks associated with transfusion.

The use of automated platforms, microarray methods, and massively parallel sequencing is becoming more prevalent across both developed and developing markets, as they provide scalability, reduced labor costs, and faster throughput. These improvements are particularly crucial in resource-constrained settings, where accurate and quick diagnostics can be lifesaving.

Despite robust growth, the industry is not without challenges. The risks associated with blood transfusions—including acute and delayed hemolytic reactions, allergic responses, and fevers—necessitate rigorous testing protocols. These complications can arise when there’s a mismatch in blood types, underscoring the need for high-performance reagents.

Furthermore, acute hemolytic reactions can trigger immune responses against transfused red blood cells, leading to serious health implications. As a result, the demand for blood-grouping reagents is further bolstered by their role in preventing such complications through reliable blood type matching.

A comprehensive analysis identifies the following as the key players shaping the blood-grouping reagents market:

Arena Bio Science

ARKRAY Inc.

Atlas Medical GmbH

BAG Health Care GmbH

Bio-Rad Laboratories Inc.

Calibre Scientific Inc.

Danaher Corp.

DIAGAST SAS

Fortress Diagnostics

Grifols SA

Merck KGaA

Novacyt SA

Paragon Care Group

QuidelOrtho Corp.

Rapid Labs Ltd.

Thermo Fisher Scientific Inc.

Torax Biosciences Ltd.

Tulip Diagnostics Pvt. Ltd.

These companies are evaluated on their innovation pipeline, strategic focus, and market influence. The industry analysis classifies them into pure play, category-focused, industry-focused, and diversified organizations. Quantitative rankings further categorize them as dominant, leading, strong, tentative, or weak in the current market landscape.

For more details about the industry, get the PDF sample report for free

The Blood-Grouping Reagents Market is driven by increasing demand for blood typing reagents, monoclonal antibodies, and antiserum reagents across diagnostic and clinical settings. Techniques such as ABO typing, Rh typing, and antigen detection are foundational in ensuring transfusion compatibility and accurate blood donation screening. Key reagents like reagent red cells, phenotyping reagents, rare antisera, and quality control reagents are utilized in routine immunohematology testing to identify blood group antigens and perform antibody screening using advanced serology tests. The adoption of automated analyzers, rapid test kits, gel card technology, and microplate systems is accelerating the pace and reliability of blood typing workflows in hospitals and blood banks. In addition to traditional Coombs test methods like direct antiglobulin and indirect antiglobulin, serological fluids and enzyme reagents are essential components of modern blood grouping systems, especially for managing emergencies and chronic disease-related transfusions.

Innovative testing platforms are transforming clinical diagnostics in the blood-grouping reagents market, with molecular methods such as PCR-based typing, microarray techniques, and massively parallel sequencing gaining momentum for high-resolution molecular tests. These technologies are enhancing transfusion diagnostics, particularly for complex cases requiring precise cross-matching reagents. The rise of assay-based methods and nucleic acid testing further enables healthcare providers to offer reliable blood safety testing and donor compatibility analysis. The demand for high-throughput blood typing instruments, coupled with the need for dependable diagnostic kits, is contributing to the expansion of the market across various laboratory reagents segments. Moreover, increased reliance on reagent consumables and automated systems is optimizing workflow efficiency and traceability in critical transfusion services. These advances are vital in supporting national blood programs and ensuring the integrity of blood supplies worldwide.

Get more details by ordering the complete report

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.