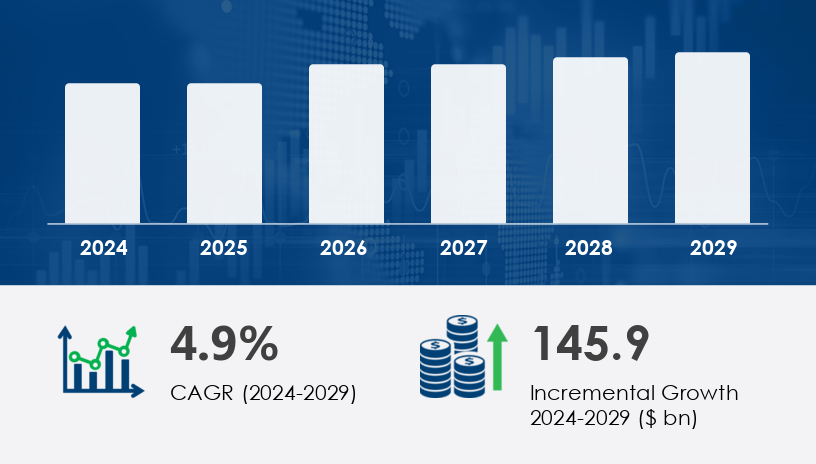

The global animal feed market is poised for significant expansion, with projections indicating an increase of USD 145.9 billion between 2024 and 2029, reflecting a compound annual growth rate (CAGR) of 4.9%. This growth is primarily driven by escalating global meat consumption, technological advancements in feed production, and a shift towards sustainable and alternative feed sources. However, the industry faces challenges such as the high cost of non-GMO feed and stringent regulatory environments, particularly in developed regions like the North America and Europe.

For more details about the industry, get the PDF sample report for free

A central driver propelling the growth of the animal feed market is the rising investment and expansion in production capacity to meet the increasing demand for meat. Population growth, coupled with shifting consumer dietary preferences, has amplified the need for affordable and consistent protein sources. A notable example is De Heus, a Koudijs subsidiary, which invested USD 5.3 million in a Ukrainian feed additive facility in 2023, focused on high-quality vitamin and mineral blends. This strategic investment highlights the industry’s push toward expanding operations and maintaining competitiveness amid rising global protein consumption.

An emerging trend in the animal feed market is the rise in global meat consumption, especially in poultry. According to the OECD, global meat production hit 340 million tons in 2023, up from nearly 248 million tons in 2021, with poultry witnessing a remarkable 16% growth between 2013 and 2023. This shift aligns with increasing health consciousness and higher protein intake in diets. As populations grow and sustainable food becomes a global priority, the demand for nutritionally optimized animal feed continues to rise, spurring innovation in feed formulation and sustainability practices.

The Animal Feed Market is evolving rapidly with a diverse portfolio of offerings including liquid feed, dry feed, and customized feed additives that enhance animal performance and productivity. Key innovations such as organic supplements, trace minerals, and probiotic feed are driving a shift toward health-conscious and sustainable farming practices. Functional ingredients like enzymatic additives, amino acids, feed enzymes, and feed acidifiers are widely adopted to boost digestion, nutrient uptake, and disease resistance. Common base materials such as cereal grains, protein meals, milk replacer, soybean meal, corn feed, and wheat products serve as essential energy and protein sources in modern feed formulations.

The animal feed market is segmented by:

Type: Poultry, Swine, Ruminant, Aquaculture, Others

Product: Pellets, Mash, Crumbles

Source: Cereals, Protein sources, Additives

Among all segments, the poultry feed segment leads the market due to the surging demand for poultry meat. Valued at USD 189.60 billion in 2019, the segment has demonstrated steady growth and is expected to dominate through 2029. The expansion of poultry production to meet global meat consumption is fueling the demand for specialized poultry feeds. According to analysts, sustainability, animal welfare, and feed safety are crucial pillars in this segment, supported by innovations in precision feeding, grain processing, and feed traceability.

See What’s Inside: Access a Free Sample of Our In-Depth Market Research Report.

Covered Regions:

North America (US, Canada)

Europe (Germany, UK)

APAC (China, India, Japan, South Korea, Australia)

South America (Brazil)

Middle East and Africa

Asia-Pacific (APAC) is the leading region, contributing 50% to the global market growth between 2024 and 2029. Countries like India and China have a large livestock population and growing demand for beef, chicken, and veal. Numerous feed mills and technological advancements like remote monitoring, feed traceability, and digital agriculture support this growth. Analysts note that APAC’s market is also being driven by the adoption of organic and non-GMO feed, reflecting consumers' growing focus on health, safety, and sustainability in animal nutrition.

A major challenge in the animal feed market is the high cost of non-GMO animal feed, which restricts affordability for some farmers. Non-GMO feed, perceived as healthier and more sustainable, often carries a premium of 40% to 50% in profit margins. While this appeals to a segment of health-conscious consumers, it also creates barriers for broader market penetration, particularly in price-sensitive regions. The rising preference for non-GMO options emphasizes the need for manufacturers to balance cost-efficiency with quality and traceability.

Alternative protein sources are reshaping the market landscape, with growing use of insect meal, algae-based feed, and plant-based feed to promote sustainable feed practices. The demand for non-GMO feed is also rising as consumers seek transparency and cleaner supply chains. In terms of physical forms, feed pellets, feed crumbles, and feed mash are manufactured to suit the species-specific requirements of livestock and pets. Supplemental forms like premixes, oral powder, and oral solutions are being adopted for targeted nutrition and precise dosage. These solutions support feed formulation goals that prioritize nutrient absorption, gut health, and feed efficiency across species

Growing concerns about antibiotic resistance and food safety have led to an increase in antibiotic-free feed options and innovations aimed at improving feed conversion and livestock nutrition. Parallel demand growth in the pet food and aquafeed sectors is driving the need for precision feeding strategies and high-quality feed ingredients tailored to each species. With regulatory bodies emphasizing feed safety and nutritional consistency, feed producers are integrating technology and data analytics to create smart, traceable supply chains. The Animal Feed Market is thus poised for significant transformation, balancing productivity with sustainability in an increasingly conscious global ecosystem.

Leading players in the animal feed market are pursuing strategic alliances, acquisitions, and product launches to expand their global footprint. Companies like Adis France SAS focus on high-quality ruminant meat feed, fortified with vitamins and minerals to support animal immunity. Technological advancements such as feed formulation software, feed processing automation, and nutrient optimization are being adopted widely. Precision livestock farming and data analytics are also enhancing feed efficiency and disease prevention, positioning innovation as a core competitive advantage.

Adis France SAS

Alltech Inc.

Archer Daniels Midland Co.

Associated British Foods Plc

BASF SE

Biochem Additives and Product mbH

BRF

Cargill Inc.

Charoen Pokphand Foods PCL

Chr Hansen AS

Corbion nv

Evonik Industries AG

International Flavors and Fragrances Inc.

Jefo

Kemin Industries Inc.

Kent Nutrition Group Inc.

Land O Lakes Inc.

New Hope Group Co. Ltd

Executive Summary

Market Landscape

Market Sizing

Historic Market Size

Five Forces Analysis

Market Segmentation

6.1 Type

6.1.1 Poultry

6.1.2 Swine

6.1.3 Ruminant

6.1.4 Aquaculture

6.1.5 Others

6.2 Product

6.2.1 Pellets

6.2.2 Mash

6.2.3 Crumbles

6.3 Source

6.3.1 Cereals

6.3.2 Protein Sources

6.3.3 Additives

6.4 Geography

6.4.1 North America

6.4.2 APAC

6.4.3 Europe

6.4.4 South America

6.4.5 Middle East and Africa

Customer Landscape

Geographic Landscape

Drivers, Challenges, and Trends

Company Landscape

Company Analysis

Appendix

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.