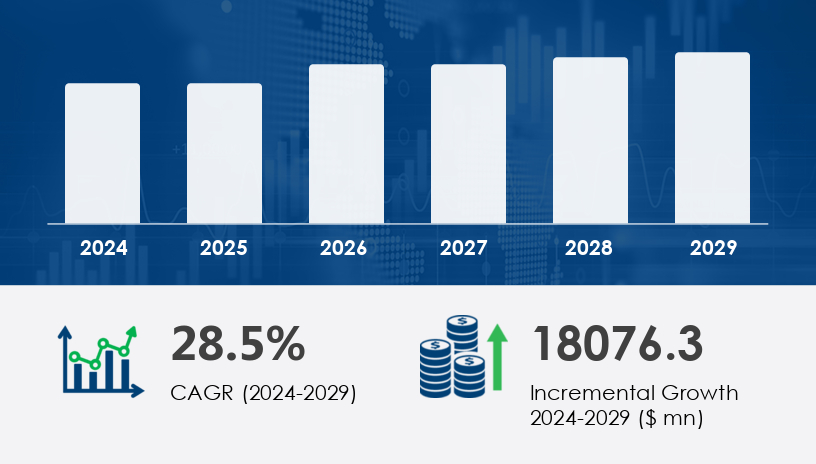

The global surgical robots market is poised for robust expansion, projected to grow by USD 18.08 billion by 2029, driven by a compound annual growth rate (CAGR) of 28.5%. This growth is fueled by technological advancements, rising demand for minimally invasive procedures, and global healthcare infrastructure investments. As healthcare systems worldwide adopt robotic solutions to enhance precision and patient outcomes, the market is gaining momentum across developed and emerging regions.

For more details about the industry, get the PDF sample report for free

One of the primary drivers propelling growth in the surgical robots market is the surging demand for minimally invasive surgeries, particularly in the United States and Europe. These procedures result in faster recovery times, lower post-operative complications, and reduced hospital stays. Robotic systems such as Intuitive Surgical’s da Vinci have become increasingly prevalent for general and urological surgeries, transforming surgical protocols. A compelling example is a hospital in California that adopted the da Vinci Xi for urological procedures and achieved a 40% reduction in patient recovery time, emphasizing the transformative role of surgical robotics in enhancing procedural efficiency and patient care.

The market is rapidly evolving with key technological innovations. A standout trend is the integration of AI-driven surgical planning, enhancing procedural precision and reducing complications. In the United States, AI algorithms embedded in surgical robots analyze patient data for optimized movement and decision-making during neurosurgeries. Simultaneously, 5G-enabled remote surgeries are gaining traction, with Japan piloting thoracic operations through low-latency networks. This innovation is expanding surgical access to rural and underserved populations, especially in China and the UAE. These trends are ushering in a new era of precision medicine and global surgical reach, reshaping the capabilities of modern healthcare.

The Surgical Robots Market is rapidly evolving with technological advancements driving the adoption of robotic systems in various procedures such as general surgery, orthopedic surgery, cardiac surgery, and gynecologic procedures. These systems incorporate surgical arms, HD cameras, and 3D visualization to support minimally invasive approaches, enhancing surgical dexterity and precision. Robotic consoles paired with haptic feedback offer surgeons tactile responses during complex operations like brain surgery and spinal surgery, improving control and accuracy. Specialized surgical instruments, precision tools, and disposable accessories are tailored for specific interventions such as joint arthroplasty, urologic procedures, and laparoscopic surgery, while the consumables market continues to expand alongside the demand for tailored components. Additionally, vision systems and image-guided surgery technologies are boosting performance in fields such as stereotactic radiosurgery, endoscopic surgery, and cancer treatment.

The surgical robots market is segmented by:

Application: General and laparoscopy surgery, Gynecological surgery, Orthopedic surgery, Neurosurgery, Urology, Thoracic surgery, Others

End-user: Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, Academic and Research Institutions

Component: Instruments & Accessories, Robotic Systems, Maintenance and Support Services, Training and Consulting Services, Software and Connectivity Services

Among all applications, general and laparoscopy surgery stands out as the leading segment in the surgical robots market. This segment was valued at USD 1.33 billion in 2019 and continues to grow due to the rising number of global surgical procedures, estimated at 200–400 million annually. Robotic assistance enhances precision in procedures like hernia repair and cholecystectomy, especially in outpatient settings. The United States has seen rapid adoption in ambulatory centers, where robotic systems improve visualization and reduce complications. Analysts note that the increasing preference for shorter recovery times and minimally invasive techniques will sustain this segment’s dominance through 2029.

Covered Regions:

North America

Europe

Asia Pacific (APAC)

South America

Middle East and Africa

Rest of World (ROW)

North America leads the surgical robots market, contributing 39% of global growth through 2029. The region’s dominance is fueled by advanced healthcare infrastructure and rapid adoption of robotic systems like da Vinci and Mako. In the United States, approximately 129 million people suffer from chronic diseases, creating demand for minimally invasive procedures performed using robotic systems. Moreover, Canada’s orthopedic and neurosurgical sectors are increasingly adopting Stryker’s Mako system. Analysts highlight that FDA regulatory support and the region’s focus on innovation and training are accelerating adoption across hospitals and ASCs, solidifying North America’s leadership position.

See What’s Inside: Access a Free Sample of Our In-Depth Market Research Report.

Despite the market's rapid growth, high initial costs remain a significant barrier to widespread adoption. Systems like the da Vinci are priced between USD 1–2 million, making them inaccessible for smaller hospitals, particularly in countries like India and Brazil. These expenses are further compounded by installation, maintenance, and training costs, which place a heavy financial burden on healthcare facilities with limited budgets. The challenge is especially pressing in emerging markets, where infrastructure growth is outpacing affordability. Analyst insights emphasize that cost-effective, compact systems and increased funding for training are essential to address this bottleneck and unlock market potential.

Market research indicates that increasing reliance on robot-assisted surgery is fueled by a growing emphasis on patient outcomes, reduced recovery times, and enhanced surgical precision. The integration of AI and machine learning into surgical software allows for real-time imaging, predictive analytics, and adaptive movements in delicate procedures. Innovations such as cloud robotics and telesurgery platforms have further enabled remote surgery, expanding access in underserved regions. Extensive training programs and surgical simulators are critical to developing proficiency in preoperative planning, surgical navigation, and intraoperative decision-making. The rise in neurosurgery robots and medical imaging advancements continues to support complex procedures that benefit from precise planning and feedback systems. These developments are further supported by robust data collection through surgical analytics, fostering continuous improvements in robotic-assisted medical care.

The research analysis of the surgical robots market reveals a dynamic landscape shaped by multi-disciplinary innovation and clinical demand. Emphasis on improving surgical efficacy through AI integration, feedback-rich interfaces, and real-time decision support tools highlights the critical role of advanced robotics in the future of surgery.

The surgical robots market is witnessing an influx of innovations and strategic developments among key players to stay ahead in a rapidly evolving landscape. Companies such as Intuitive Surgical, Medtronic, and Stryker are spearheading advancements in AI integration, haptic feedback, and compact system design. For instance, Stryker’s Mako system leverages AI-driven planning to enhance implant placement accuracy in orthopedic procedures, achieving a 30% improvement in precision at a hospital in Mumbai. Meanwhile, Medtronic’s Hugo RAS system, known for its compact footprint, is gaining traction in ambulatory surgical centers across the UK and India, thanks to its cost-efficiency. Training initiatives using virtual reality are also being implemented by U.S. and French institutions to bridge the surgeon skill gap. Furthermore, the development of eco-friendly and sustainable robotic components, especially in France and Canada, reflects a growing emphasis on environmental responsibility within the industry.

1. Executive Summary

2. Market Landscape

3. Market Sizing

4. Historic Market Size

5. Five Forces Analysis

6. Market Segmentation

6.1 Application

6.1.1 General and laparoscopy surgery

6.1.2 Gynecological surgery

6.1.3 Orthopedic surgery

6.1.4 Neurosurgery

6.1.5 Urology

6.1.6 Thoracic surgery

6.1.6 Others

6.2 End-user

6.2.1 Hospitals

6.2.2 Ambulatory service centers

6.2.3 Specialty Clinics

6.2.4 Academic and Research Institutions

6.3 Component

6.3.1 Instruments & Accessories

6.3.2 Robotic Systems

6.3.3 Maintenance and Support Services

6.3.4 Training and Consulting Services

6.3.5 Software and Connectivity Services

6.4 Geography

6.4.1 North America

6.4.2 APAC

6.4.3 Europe

6.4.4 South America

6.4.5 Middle East And Africa

7. Customer Landscape

8. Geographic Landscape

9. Drivers, Challenges, and Trends

10. Company Landscape

11. Company Analysis

12. Appendix

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.