The Semiconductor Foundry Market is being driven by Increasing demand for IoT in business

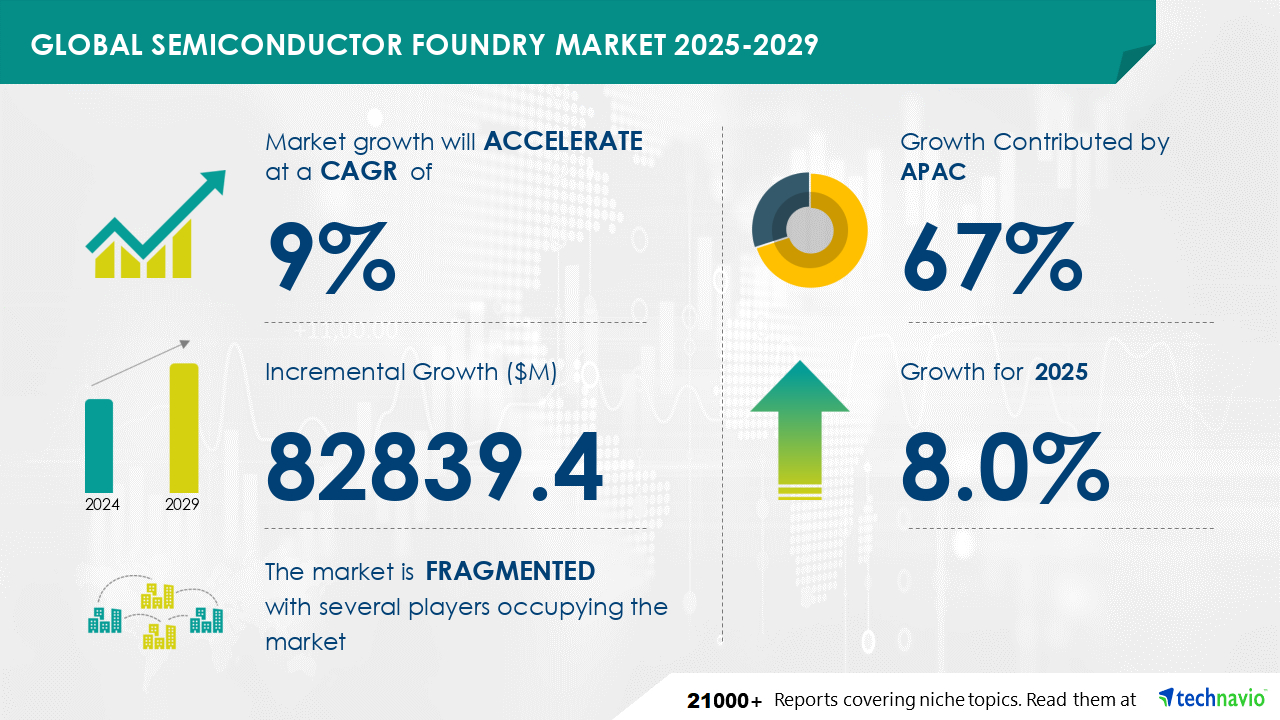

The Semiconductor Foundry Market is expected to grow at a CAGR of 9% during 2024 and 2029. During this period, the market is also expected to show a growth of USD 82839.4 million. Semiconductor foundries are leveraging big data to optimize their operations and make informed business decisions. With the integration of sensors and data-collecting devices in their manufacturing processes, foundries are able to gather vast amounts of data from various tools within their fabs. This data is analyzed using advanced analytics to enable predictive maintenance, advanced process controls, and intelligent scheduling. By simplifying the manufacturing process through data-driven insights, semiconductor foundries are enhancing their overall efficiency and competitiveness in the market.

Get more information on Semiconductor Foundry Market by requesting a sample report

The market is segmented based on

According to Technavio, There are several factors that are causing the market to flourish during the forecast period, which are as follows:

However, the market also witnesses some limitations, which are as follows:

Rich Experience: 20+ years leading global market research, trusted insights across industries.

Unlock Business Potential with Technavio: Maximize ROI with Technavio's tailored market research: deep dives and actionable insights.

Your Guide to Market Success: Empower your business with Technavio's market research and future-proof your decisions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

231 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9% |

|

Market growth 2025-2029 |

USD 82839.4 million |

|

Market structure |

fragmentation |

|

YoY growth 2024-2025(%) |

8.0 |

|

Key countries |

Taiwan, US, China, Japan, South Korea, Germany, India, France, Canada, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Find out which segment is leading the market by accessing the free PDF report

The Semiconductor Foundry Market encompasses the production of silicon wafers, involving thin film deposition of dielectric and conductive materials. This process leads to packaging design, utilizing lead-free packaging for thermal management and power consumption reduction. Performance optimization, reliability testing, and failure analysis ensure yield enhancement through process and manufacturing automation. Advanced materials, computational design, and process simulation are integral, along with semiconductor equipment like lithography, etching, and deposition systems. Metrology equipment, yield management software, design software, process control software, and industry standards govern the global semiconductor industry, influenced by the semiconductor supply chain, geopolitical factors, and government regulations.

In the dynamic landscape of the global semiconductor market, semiconductor foundries play a pivotal role as key providers of wafer fabrication services to integrated device manufacturers (IDMs), fabless companies, and original equipment manufacturers (OEMs) and original design manufacturers (ODMs). The market's growth is underpinned by significant investments in semiconductor fabrication facilities, with a focus on yield optimization, process control, defect analysis, and advanced packaging. Technavio's market analysis indicates that this trend will continue, driven by the increasing demand for semiconductor ICs in various industries, including consumer electronics, automotive, industrial automation, and telecommunications. As a result, semiconductor foundries are prioritizing innovation and efficiency in their operations to meet the evolving needs of their clients and maintain a competitive edge.. Industries are leveraging the products belonging to the market for customer engagement, transactional notifications, and promotional offers.

Technavio Research

Jesse Maida

Media & Marketing Executive

US: +1 844 364 1100

UK: +44 203 893 3200

Email: media@technavio.com

Website: www.technavio.com/

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.