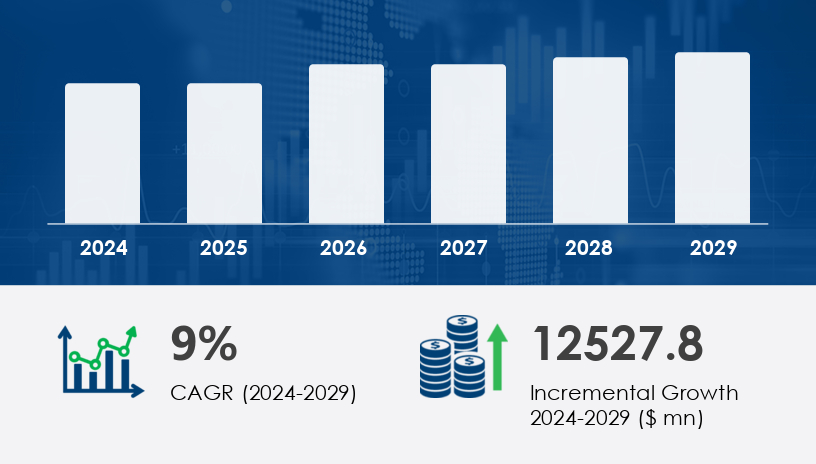

The Japan Semiconductor Device Market is poised for robust growth from 2025 to 2029, fueled by increasing investments in advanced technologies and the rising demand across consumer and industrial sectors. Japan remains a crucial hub for semiconductor innovation, with significant contributions in 5G, AI, and power electronics.In 2024, the Japan semiconductor device market was valued at approximately USD 34.8 billion. It is forecast to increase by USD 12.53 billion by 2029, growing at a CAGR of 9% over the forecast period.

Explore trends, segmentation, and growth drivers: View Free Sample PDF

One of the primary drivers for the Japan Semiconductor Device Market is the growing demand for high-power density devices across industries such as automotive, industrial automation, and renewable energy. Wide-bandgap semiconductors like silicon carbide (SiC) and gallium nitride (GaN) are increasingly being deployed due to their superior performance at high temperatures (up to 500°C) and voltage ranges. These materials enable efficient energy use in electric vehicles, UPS systems, and photovoltaic inverters, leading to enhanced switching speed, reduced power loss, and higher thermal tolerance. Their adoption is critical in addressing the rising power efficiency demands of modern electronics.

A significant trend reshaping the Japan Semiconductor Device Market is the surging investment in 5G infrastructure and related technologies. As Japan accelerates its transition into Industry 4.0, the integration of 5G is unlocking new applications in industrial automation, smart cities, and connected healthcare. Semiconductor materials such as silicon carbide are gaining prominence for their ability to improve power efficiency in telecom and AI-driven systems. Meanwhile, miniaturization and cleanroom innovation are enhancing the transistor density and process optimization, vital for AI, neuromorphic computing, and quantum computing. The ongoing focus on transistor architecture innovation and heterogeneous integration highlights the transformative direction of the industry.

The Japan Semiconductor Device Market is characterized by a strong foundation in core component manufacturing, particularly in silicon wafers, integrated circuits, and microchip design. As consumer electronics, automotive, and industrial applications expand, there’s increasing demand for high-performance transistor arrays, memory chips, flash storage, DRAM modules, and NAND flash technologies. Japan continues to lead in the development of both logic devices and analog circuits, while innovations in power semiconductors—including MOSFET transistors, IGBT modules, and thyristor devices—are crucial for electric vehicle and smart grid deployments. Additionally, diode arrays, sensor chips, and MEMS devices are widely used in automation and IoT applications. The rise of high-frequency applications has boosted the adoption of RF amplifiers, GaN semiconductors, and SiC wafers, reinforcing Japan’s prominence in advanced material integration.

The Japan Semiconductor Device Market is segmented by:

Application

Consumer Electronics

Communications

Automotive

Medical Devices

Others

Device

PMIC (Power Management IC)

Microchips

RFID

Material

Silicon

Germanium

Gallium Arsenide

Others

Geography

APAC

Japan

Among all segments, consumer electronics holds the largest share and is expected to witness significant growth through 2029. This expansion is driven by the increased adoption of smartphones, smart TVs, gaming consoles, and laptops, which depend heavily on memory chips and power management ICs. The report indicates that GaAs components, essential for handset power amplifiers, will experience heightened demand due to rising global smartphone shipments. Moreover, the segment benefits from design automation and yield enhancement, supporting the industry's transition toward higher transistor density and energy-efficient architectures. Analysts highlight that machine learning and AI integration are reinforcing demand for digital signal processors and application-specific integrated circuits (ASICs) in consumer devices.

APAC, particularly Japan, leads the semiconductor device market in terms of both market share and technological innovation. Japan's deep-rooted semiconductor ecosystem and investments in 5G infrastructure have positioned it as a regional hub. The integration of semiconductors in industrial automation, healthcare wearables, and autonomous vehicles has propelled growth. The market in Japan is projected to grow by USD 12.53 billion between 2024 and 2029. In addition, the adoption of GaN and SiC materials, advanced chip packaging, and smart home technologies have accelerated regional expansion. Analysts underscore that Japan's edge in cleanroom technology and semiconductor manufacturing equipment further strengthens its competitive advantage.

See What’s Inside: Access a Free Sample of Our In-Depth Market Research Report.

A major challenge confronting the Japan Semiconductor Device Market is the high cost of semiconductor devices, especially those using SiC and GaN substrates. For instance, a 100 mm GaN wafer costs approximately USD 1,800, while a 100 mm SiC wafer exceeds USD 2,000, compared to just USD 19.02 for a 125 mm Si wafer. The substrate cost alone accounts for over 30% of the total cost in SiC-based devices, making them five times more expensive than conventional silicon semiconductors. This price gap limits mass adoption and complicates the pricing strategies of device manufacturers. Although innovations in chip design, machine learning, and alternative materials aim to reduce costs, affordability remains a significant barrier.

A growing emphasis on computational efficiency and energy optimization has driven the development of specialized chips in Japan, such as ASIC chips, FPGA devices, and SoC architectures—all of which support high-end consumer and industrial systems. Core processing technologies like CPU cores, GPU units, microcontroller units, and DSP processors are vital in Japan’s consumer electronics and embedded systems market. Meanwhile, the optoelectronic segment is thriving with innovations in LED chips, photodiode sensors, and CMOS sensors, contributing significantly to imaging and lighting advancements. Japan is also exploring futuristic designs like quantum dots and neuromorphic chips, as well as photonics ICs, which are expected to revolutionize high-speed data transmission. To ensure device functionality and safety, the market supports robust solutions in power ICs, voltage regulators, battery management systems, and RF filters, making Japan a comprehensive player across all semiconductor domains.

The continued evolution of the Japan Semiconductor Device Market is shaped by the integration of multifunctional platforms such as antenna modules, mixed-signal ICs, and embedded processors, which are foundational to both communication and control systems. Supporting next-generation hardware architectures, components like gate drivers, Schottky diodes, and other discrete semiconductors enhance switching performance, power efficiency, and system reliability. Japan's innovation-driven approach, backed by a legacy of precision manufacturing and high R&D investment, enables the market to stay competitive and forward-looking across the global semiconductor landscape.

Companies operating in the Japan Semiconductor Device Market are adopting diverse strategies to maintain competitiveness:

Advanced Micro Devices Inc. offers a broad range of low-power, high-performance FPGAs for industrial and defense applications.

NVIDIA Corp., Intel Corp., and Samsung Electronics Co. Ltd. are investing heavily in AI chipsets and heterogeneous integration.

Mitsubishi Electric, ROHM Co. Ltd., and Renesas Electronics are focusing on automotive-grade semiconductors.

Partnerships and strategic alliances with OEMs and fabless companies are enabling firms to access niche markets and expand their R&D capabilities.

Recent innovations include 3D integration, LED lighting applications, solar energy harvesting solutions, and advanced packaging that enhance device functionality while optimizing space and thermal management.

The Japan Semiconductor Device Market is undergoing a dynamic transformation driven by technological advancements and increasing demand from various sectors. With a projected CAGR of 9%, the market is set to grow by USD 12.53 billion by 2029. Key growth drivers such as high-power density device adoption and 5G infrastructure expansion are unlocking new opportunities. However, cost-related barriers remain a significant hurdle. Through innovation in materials, chip architecture, and strategic partnerships, market leaders are well-positioned to navigate challenges and capitalize on Japan's semiconductor renaissance

Executive Summary

Market Landscape

Market Sizing

Historic Market Size

Five Forces Analysis

Market Segmentation

6.1 Application

6.1.1 Consumer Electronics

6.1.2 Communications

6.1.3 Automotive

6.1.4 Medical Devices

6.1.5 Others

6.2 Device

6.2.1 PMIC

6.2.2 Microchips

6.2.3 RFID

6.3 Material

6.3.1 Silicon

6.3.2 Germanium

6.3.3 Gallium Arsenide

6.3.4 Others

6.4 Geography

6.4.1 APAC

6.4.2 Japan

Customer Landscape

Geographic Landscape

Drivers, Challenges, and Trends

Company Landscape

Company Analysis

Appendix

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.