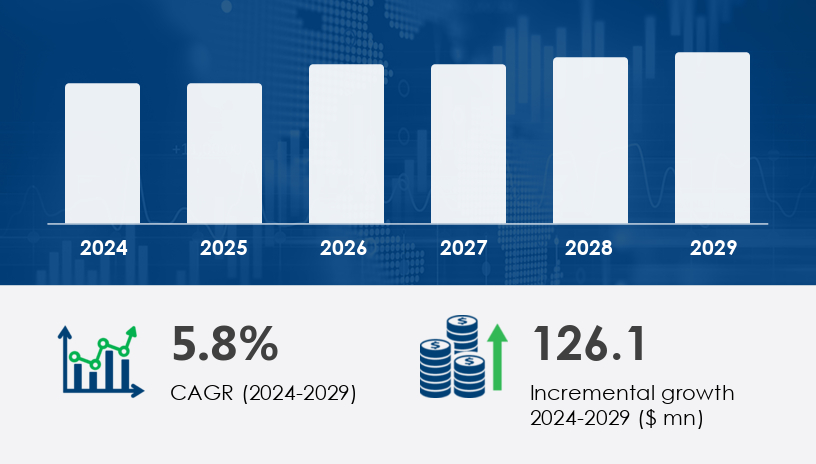

The Non-Invasive Intracranial Pressure Monitoring Devices Market is experiencing steady growth driven by the increasing prevalence of neurological conditions and demand for safer alternatives to traditional invasive monitoring. These devices allow for real-time intracranial pressure (ICP) assessments without surgical intervention, improving outcomes for patients suffering from conditions such as traumatic brain injuries, hydrocephalus, and intracranial tumors.In 2024, the market was valued at approximately USD 126.1 billion. It is projected to expand at a CAGR of 5.8%.For more details about the industry, get the PDF sample report for free

A primary driver fueling the growth of the non-invasive intracranial pressure monitoring devices market is the growing awareness of non-invasive technologies in neurocritical care. Unlike traditional invasive methods, which involve inserting a catheter into the brain—posing risks such as infection and hemorrhage—non-invasive ICP devices offer a safer, more efficient option. These include techniques like transcranial doppler ultrasonography, MRI/CT, and devices like the Cerepress HS-1000M Monitor. The need to monitor ICP in patients with traumatic brain injuries, hydrocephalus, and meningitis—especially in trauma and postoperative care—has significantly increased. Healthcare providers are increasingly adopting portable and wireless systems, which enhance patient monitoring capabilities in both hospital and home settings.

An emerging trend in the market is the integration of artificial intelligence (AI) and machine learning (ML) into ICP monitoring systems. These advanced technologies enhance clinical decision-making by offering real-time analytics and enabling early diagnosis of complications. Additionally, growing R&D investments and regulatory approvals are bolstering innovation in the sector. For instance, SanBio Co., Ltd. received marketing approval in Japan for a novel stem cell-based product to address motor paralysis from traumatic brain injury. This trend illustrates how cutting-edge, minimally invasive techniques are reshaping the landscape of neurocritical care, offering better patient outcomes and reducing long-term healthcare costs.

The Non-Invasive Intracranial Pressure (ICP) Monitoring Devices Market is witnessing significant growth as the global burden of traumatic brain injury, ischemic stroke, intracerebral hemorrhage, and subarachnoid hemorrhage continues to rise. Conditions such as meningitis, hydrocephalus, intracranial tumors, and brain infections demand rapid and accurate assessment of brain pressure to avoid complications. Non-invasive approaches using technologies like Transcranial Doppler, MRI-based monitoring, and CT monitoring are gaining popularity in neurointensive care and trauma care settings. Devices such as Cerepress and HS-1000M Monitor, along with advanced ultrasound probes, offer real-time insights into cerebrospinal fluid dynamics and cerebrovascular autoregulation. These innovations improve outcomes in high-risk populations, particularly in road accidents, sports injuries, and the elderly population.

The Non-Invasive Intracranial Pressure Monitoring Devices Market is segmented by:

Application:

Traumatic Brain Injury

Intracerebral Hemorrhage

Subarachnoid Hemorrhage

Meningitis

Others

Geography:

North America (US, Canada, Mexico)

Europe (Germany, UK, France)

Asia (China, India, Japan)

Rest of the World (ROW)

Among all application segments, traumatic brain injury (TBI) remains the most dominant, both in terms of revenue and projected growth. In 2019, this segment was valued at USD 149.20 billion and has shown steady growth throughout the forecast period. TBIs result from events like road accidents, sports injuries, and falls, all of which require constant and accurate monitoring of ICP. Non-invasive solutions are being increasingly adopted in neurocritical care settings due to their ability to monitor physiological changes without invasive procedures. According to analysts, the growing recognition of non-invasive ICP monitoring in managing TBIs is leading hospitals, clinics, and diagnostic laboratories to invest heavily in advanced monitoring systems for improved trauma care.

Regions Covered:

North America

Europe

Asia-Pacific (APAC)

Latin America

Middle East & Africa (MEA)

Rest of the World (ROW)

North America dominates the Non-Invasive Intracranial Pressure Monitoring Devices Market, contributing approximately 54% of the global market growth during the forecast period. This growth is attributed to the high incidence of neurological conditions, increased healthcare spending, and a strong emphasis on minimally invasive surgical techniques. The region benefits from advanced healthcare infrastructure, widespread clinical adoption of transcranial doppler, MRI/CT technologies, and robust demand for wireless monitoring systems. As per Technavio analysts, North America’s consistent investments in AI-enabled diagnostic solutions and trauma care technologies significantly bolster the adoption of non-invasive ICP monitoring, further strengthening its market leadership.

Despite the rising adoption, the market faces a major hurdle in the continued availability and reliance on invasive ICP monitoring techniques. Many healthcare providers, especially in developing regions, still utilize traditional methods such as ventriculostomy and fiberoptic catheterization, largely due to established clinical protocols and initial cost barriers associated with transitioning to newer systems. These invasive techniques, though effective, increase the risk of infection, hemorrhage, and longer hospital stays. The persistence of these older systems slows down the full-scale adoption of next-generation non-invasive technologies, highlighting the need for better education, cost-reduction strategies, and broader accessibility to advanced devices.

Driven by the shift toward non-invasive devices, the market is expanding across critical care, neurosurgery tools, and patient management applications. Tools that measure optic nerve sheath diameter or analyze blood flow in the ophthalmic artery are critical in early diagnosis and intervention. Additionally, the integration of telemedicine, wireless monitoring, and portable monitoring allows for continuous monitoring and improves access to care, especially in remote or underserved regions. Emerging innovations like robotic catheters support minimally invasive diagnostics, while the rise of machine learning and artificial intelligence in clinical decision-making enables dynamic monitoring and predictive analysis for personalized treatment plans.

In response to the growing incidence of neurological disorders, hospitals and research institutions are investing in clinical trials focused on improving real-time monitoring technologies. The synergy of AI, machine learning, and smart sensors is transforming the landscape of non-invasive brain pressure diagnostics. These technologies help assess optic nerve signals, sheath diameter changes, and blood flow metrics in a non-intrusive manner, enabling more accurate and faster treatment pathways. Moreover, with the demand for enhanced safety in trauma care, neurointensive care, and clinical decision-making, the market is poised for continued innovation and integration into next-generation diagnostic platform

Leading companies in the market are actively pursuing strategic alliances, product launches, and technological upgrades to gain a competitive edge. Major players include:

Medtronic Plc

Integra LifeSciences Holdings Corp.

Compumedics Ltd.

Johnson & Johnson Inc.

Natus Medical Inc.

Nihon Kohden Corp.

Sophysa

Spiegelberg GmbH & Co. KG

RAUMEDIC AG

Many of these companies are investing in wireless and portable non-invasive ICP monitoring systems, which enable real-time data analysis and integration with hospital information systems. For example, robotic-controlled catheters and AI-driven monitoring devices are reshaping neurocritical care by enabling better diagnostic accuracy and decision-making. These innovations reflect the industry's transition toward smart, connected medical devices that align with modern clinical and economic goals.

Executive Summary

Market Landscape

Market Sizing

Historic Market Size

Five Forces Analysis

Market Segmentation

6.1 Application

6.1.1 Traumatic Brain Injury

6.1.2 Intracerebral Hemorrhage

6.1.3 Subarachnoid Hemorrhage

6.1.4 Meningitis

6.1.5 Others

6.2 Geography

6.2.1 North America

6.2.1.1 US

6.2.1.2 Canada

6.2.1.3 Mexico

6.2.2 Europe

6.2.2.1 Germany

6.2.2.2 UK

6.2.2.3 France

6.2.3 Asia

6.2.3.1 China

6.2.3.2 India

6.2.3.3 Japan

6.2.4 Rest of World (ROW)

Customer Landscape

Geographic Landscape

Drivers, Challenges, and Trends

Company Landscape

Company Analysis

Appendix

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.