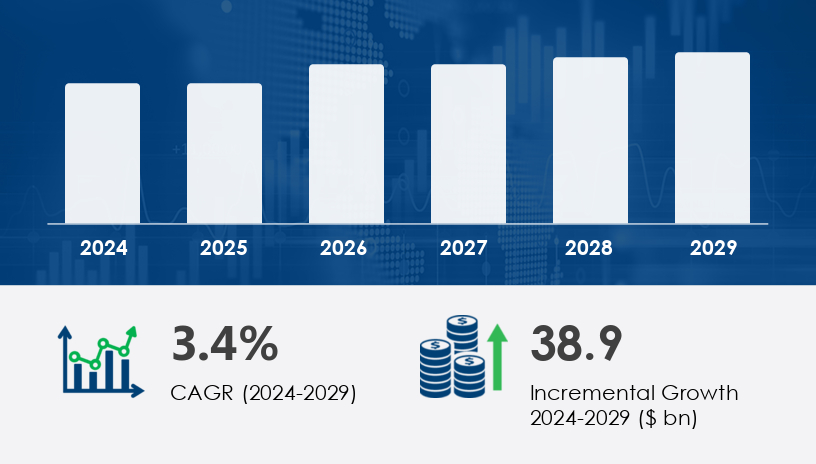

Mexico's oil and gas market is poised for significant expansion, with an anticipated increase of USD 38.9 billion from 2025 to 2029, reflecting a compound annual growth rate (CAGR) of 3.4%. This growth is underpinned by the nation's substantial hydrocarbon reserves, particularly in the Gulf of Mexico, and advancements in extraction technologies. However, the market faces challenges such as regulatory complexities, infrastructure limitations, and geopolitical risks that may impact growth trajectories.

For more details about the industry, get the PDF sample report for free

Upstream: The upstream segment is projected to experience significant growth, driven by increased exploration and production activities. Technological advancements in drilling methods, such as horizontal drilling and hydraulic fracturing, are enhancing extraction efficiency. Notable projects include the Trion deepwater development, a joint venture between Pemex and Woodside, expected to commence production in 2028.

Midstream: Investments in pipeline infrastructure and liquefied natural gas (LNG) terminals are expanding the midstream sector. The Interoceanic Corridor project, aimed at constructing a gas pipeline across the Isthmus of Tehuantepec, exemplifies such initiatives.

Downstream: The downstream sector is witnessing modernization efforts, including the construction of the Olmeca refinery, which is set to enhance gasoline and diesel production capacities. Despite these advancements, challenges persist, such as refining losses and operational inefficiencies.

Offshore: Offshore operations, particularly in the Gulf of Mexico, remain a focal point due to rich hydrocarbon reserves. Fields like Ku-Maloob-Zaap continue to be significant contributors to production volumes.

Onshore: Onshore exploration in regions such as the Sureste Basin is gaining momentum, with substantial reserves identified, including the Zama oil field.

Industrial: Industrial demand for energy is escalating, driven by manufacturing and production activities. Natural gas is increasingly utilized as a cleaner alternative to other fossil fuels.

Commercial and Residential: Urbanization is leading to higher energy consumption in commercial and residential sectors, further propelling demand for oil and gas products.

Crude Oil: Crude oil production remains a cornerstone of Mexico's energy sector, with significant contributions from offshore fields.

Refined Petroleum Products: The demand for refined products is on the rise, necessitating enhancements in refining capacities.

Natural Gas: Natural gas is gaining prominence as a transitional fuel, aligning with global decarbonization efforts.

Exploration and Drilling Equipment: Advancements in drilling technologies are pivotal for accessing both conventional and unconventional reserves.

Refining and Petrochemical Processing: Modernization of refining processes is crucial to meet growing demand and improve efficiency.

Pipeline Infrastructure and Transportation: Developing robust pipeline networks is essential for efficient distribution and export of hydrocarbons.

Storage and Distribution: Enhancements in storage facilities and distribution networks are necessary to accommodate increasing production volumes.

See What’s Inside: Access a Free Sample of Our In-Depth Market Research Report.

Abundant Resource Potential: Mexico's proven reserves of approximately 6 billion barrels of oil and substantial natural gas resources position it as a key player in the global energy landscape.

Technological Advancements: Innovations in drilling and extraction technologies are enhancing production efficiency and enabling access to previously untapped reserves.

Government Policies and Investments: Supportive policies and investments in infrastructure development are fostering growth in the oil and gas sector.

Natural Gas Adoption: The shift towards natural gas as a cleaner energy source is gaining momentum, driven by environmental considerations and technological advancements.

Digitalization and Automation: The integration of digital technologies, including artificial intelligence and the Internet of Things, is optimizing operations and improving safety standards.

Petrochemical Industry Growth: Increasing demand for petrochemical products is driving investments in refining and processing capacities.

Regulatory Complexities: Bureaucratic delays and permitting challenges can impede project timelines and increase costs.

Infrastructure Limitations: Existing infrastructure may be insufficient to support the growing demands of the oil and gas sector.

Geopolitical Risks and Price Volatility: Fluctuations in global oil prices and geopolitical uncertainties can affect market stability.

Environmental Regulations: Stricter environmental policies necessitate investments in cleaner technologies and practices.

The Mexico oil and gas market is undergoing dynamic changes driven by ongoing exploration and production activities. Increased deployment of drilling rigs, advanced seismic surveys, and technologies such as hydraulic fracturing and fracking fluids are enhancing upstream capabilities. Equipment like mud pumps, drill bits, casing pipes, tubing strings, and blowout preventers are vital to safe and efficient drilling operations, supported by robust wellhead systems and completion fluids. Downhole services including wireline services, logging tools, perforating guns, and coiled tubing are playing a crucial role in well evaluation and productivity. In offshore developments, subsea manifolds and sand control mechanisms are essential. Onshore infrastructure benefits from gas compressors, pressure valves, and flow meters, while midstream efficiency is supported through pipeline pigs, storage tanks, and the development of LNG terminals to enhance gas export capabilities.

The competitive landscape of the Mexico oil and gas market is shaped by a diverse mix of global energy conglomerates and regional players, all adopting multifaceted strategies to solidify their market positions. These companies are leveraging strategic alliances, mergers and acquisitions, geographical expansion, and new product/service launches to adapt to evolving market conditions and capitalize on Mexico’s growing energy demand.

Leading companies in this market include:

Get more details by ordering the complete report

Analytical focus in the Mexican oil and gas sector is directed toward downstream advancements and operational optimization. Key technologies such as refinery catalysts, distillation units, cracking reactors, and desalting systems are being upgraded to enhance refining efficiency. Critical infrastructure like flare stacks, heat exchangers, and gas turbines are central to emissions control and energy conversion. Operational reliability is ensured by systems like SCADA systems, remote monitoring, cathodic protection, and corrosion inhibitors. Efficient extraction and processing are further supported by drilling mud, submersible pumps, ESP systems, gas separators, and precision flow control via choke valves and safety valves. Measurement accuracy is maintained using metering skids, pig launchers, and NDT testing methods. Meanwhile, upstream decision-making is enhanced through advanced reservoir modeling, ensuring more accurate forecasting and resource management in Mexico's hydrocarbon sector.

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.