The Inflammatory Bowel Disease Market is being driven by Increasing incidence of IBD worldwide

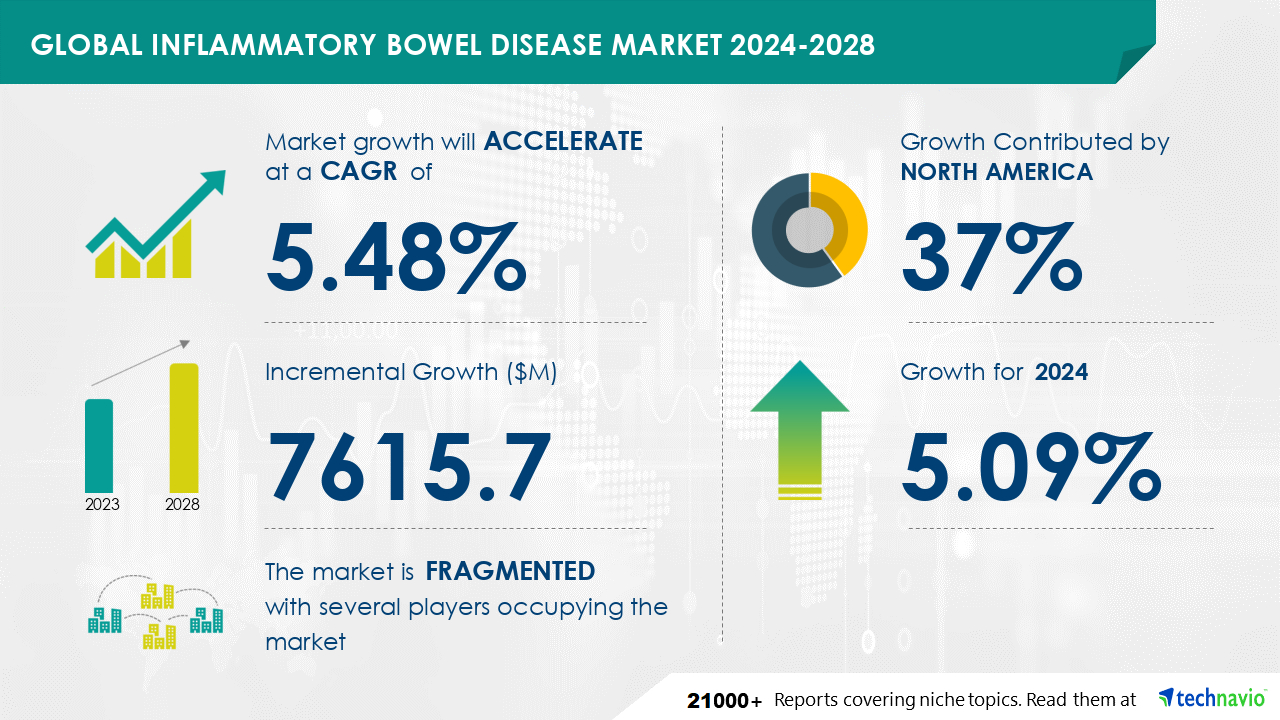

The Inflammatory Bowel Disease Market is expected to grow at a CAGR of 5.48% during 2023 and 2028. During this period, the market is also expected to show a growth of USD 7615.7 million. In the dynamic IBD market, vendors are strategically investing in research and development (R&D) to introduce innovative therapeutics, including small molecules and biologics, for managing various inflammatory bowel diseases (IBDs). Pharmaceutical and biopharmaceutical companies are increasing their R&D expenditures to bring advanced treatments to market. Notable product launches include Lupin's Mirabegron Extended-Release Tablets, 25 mg, approved by the US Food and Drug Administration (FDA) in April 2024. Additionally, in February 2021, HUMIRA (Adalimumab), a TNF blocker, secured FDA approval. These new product launches underscore the industry's commitment to delivering effective solutions for IBD patients.

Get more information on Inflammatory Bowel Disease Market by requesting a sample report

The market is segmented based on

According to Technavio, There are several factors that are causing the market to flourish during the forecast period, which are as follows:

However, the market also witnesses some limitations, which are as follows:

Rich Experience: 20+ years leading global market research, trusted insights across industries.

Unlock Business Potential with Technavio: Maximize ROI with Technavio's tailored market research: deep dives and actionable insights.

Your Guide to Market Success: Empower your business with Technavio's market research and future-proof your decisions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

170 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.48% |

|

Market growth 2024-2028 |

USD 7615.7 million |

|

Market structure |

fragmentation |

|

YoY growth 2023-2024(%) |

5.09 |

|

Key countries |

US, China, UK, India, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Find out which segment is leading the market by accessing the free PDF report

The Inflammatory Bowel Disease (IBD) market focuses on developing novel therapies for intestinal inflammation, targeting gut barrier integrity, immune cell trafficking, and inflammatory pathways. Colonic mucosa, microbiome composition, and bacterial diversity play crucial roles in IBD pathogenesis. Pathogenic bacteria and dysbiotic microbiota activate immune cells via toll-like receptors and nf-?b signaling, leading to oxidative stress, tissue damage, and the wound healing process. Intestinal microbiota, adhesion molecules, and cell signaling pathways are key areas for drug response prediction and disease progression models. Genetic risk factors and environmental triggers are also being explored as therapeutic targets. Biomarker discovery and disease severity scoring are essential for clinical trial design in IBD.

The Inflammatory Bowel Disease (IBD) market is a significant segment within the global pharmaceuticals industry, encompassing entities involved in the research and development (R&D) or production of various drug classes, including generics, non-generics, and veterinary drugs. According to Technavio's market analysis, the healthcare industry's combined revenue is calculated based on the earnings generated by manufacturers and providers of medical equipment, supplies, pharmaceuticals, biotechnology, and life sciences tools and services. The expansion of the global pharmaceuticals market will be fueled by several factors, such as the increasing elderly population. By 2050, approximately one-quarter of the US population and Europe's population ratio is projected to surpass 60 years old. This demographic shift will lead to a rise in the prevalence of age-related diseases, including IBD, which is characterized by intestinal microbiome imbalances, gut microbiota dysbiosis, inflammatory biomarkers, and mucosal immune response. These factors will create a substantial demand for pharmaceutical solutions, driving market growth.. Industries are leveraging the products belonging to the market for customer engagement, transactional notifications, and promotional offers.

Technavio Research

Jesse Maida

Media & Marketing Executive

US: +1 844 364 1100

UK: +44 203 893 3200

Email: media@technavio.com

Website: www.technavio.com/

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.