The Home Equity Lending Market is being driven by Massive increase in home prices

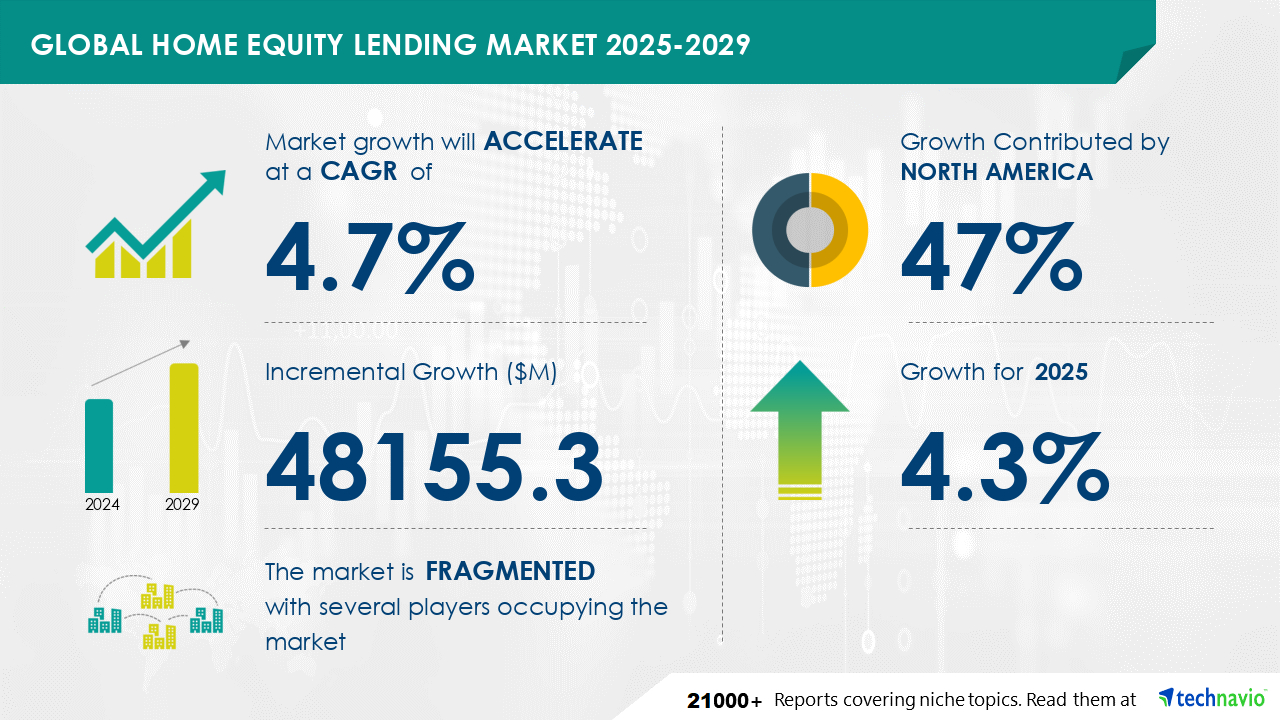

The Home Equity Lending Market is expected to grow at a CAGR of 4.7% during 2024 and 2029. During this period, the market is also expected to show a growth of USD 48155.3 million. The Indian housing sector has experienced significant growth due to the increasing population, the necessity for adequate residential and commercial infrastructure, and the shift towards nuclear families. The COVID-19 pandemic has further accelerated this trend, with an increasing number of enterprises and employees embracing remote work, leading to a surge in demand for larger homes. According to estimates, there is currently a shortage of 10 million housing units in urban areas, and this number is projected to reach 25 million by 2030 to accommodate the expanding urban population. This presents a significant opportunity for the home equity lending market to cater to the financing needs of homebuyers in India.

Get more information on Home Equity Lending Market by requesting a sample report

The market is segmented based on

According to Technavio, There are several factors that are causing the market to flourish during the forecast period, which are as follows:

However, the market also witnesses some limitations, which are as follows:

Rich Experience: 20+ years leading global market research, trusted insights across industries.

Unlock Business Potential with Technavio: Maximize ROI with Technavio's tailored market research: deep dives and actionable insights.

Your Guide to Market Success: Empower your business with Technavio's market research and future-proof your decisions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

192 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.7% |

|

Market growth 2025-2029 |

USD 48155.3 million |

|

Market structure |

fragmentation |

|

YoY growth 2024-2025(%) |

4.3 |

|

Key countries |

US, China, Germany, Japan, UK, Australia, India, France, Brazil, UAE, Rest of World (ROW), Saudi Arabia, France, South Korea, Mexico, Italy, US, China, Japan, Germany, France, UK, Australia, Canada, The Netherlands, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Find out which segment is leading the market by accessing the free PDF report

The Home Equity Lending Market employs risk mitigation strategies to address housing price fluctuations and ensure loan value security. Monetary authorities monitor interest rates to maintain housing space affordability. Second mortgages provide access to lump sum amounts for home improvements or debt consolidation, with tax deductions on interest payments. Outstanding mortgages and real estate values impact regulatory restrictions, while credit unions offer competitive rates for residential real estate loans. Homeowners consider second mortgages for high-interest debt refinancing or home improvement projects, with interest payments added to their outstanding mortgages. Housing prices, loan values, and regulatory restrictions influence the Home Equity Lending Market's dynamics.

The home equity lending market is a significant segment of the global specialized consumer services industry, encompassing revenue generated from residential mortgage services. This market is influenced by several factors, including housing prices, loan value, and interest rates. Monetary authorities play a crucial role in mitigating risks associated with home equity lending through regulatory measures. The report by Technavio quantifies the home equity lending market size based on the revenue generated by service providers offering home equity loans and lines of credit. Other specialized consumer services, such as residential services, home security services, legal services, personal services, renovation and interior design services, consumer auction services, wedding services, and funeral services, are excluded from the market analysis.. Industries are leveraging the products belonging to the market for customer engagement, transactional notifications, and promotional offers.

Technavio Research

Jesse Maida

Media & Marketing Executive

US: +1 844 364 1100

UK: +44 203 893 3200

Email: media@technavio.com

Website: www.technavio.com/

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.