The Green Petroleum Coke And Calcined Petroleum Coke Market is being driven by Increasing demand for aluminum and steel

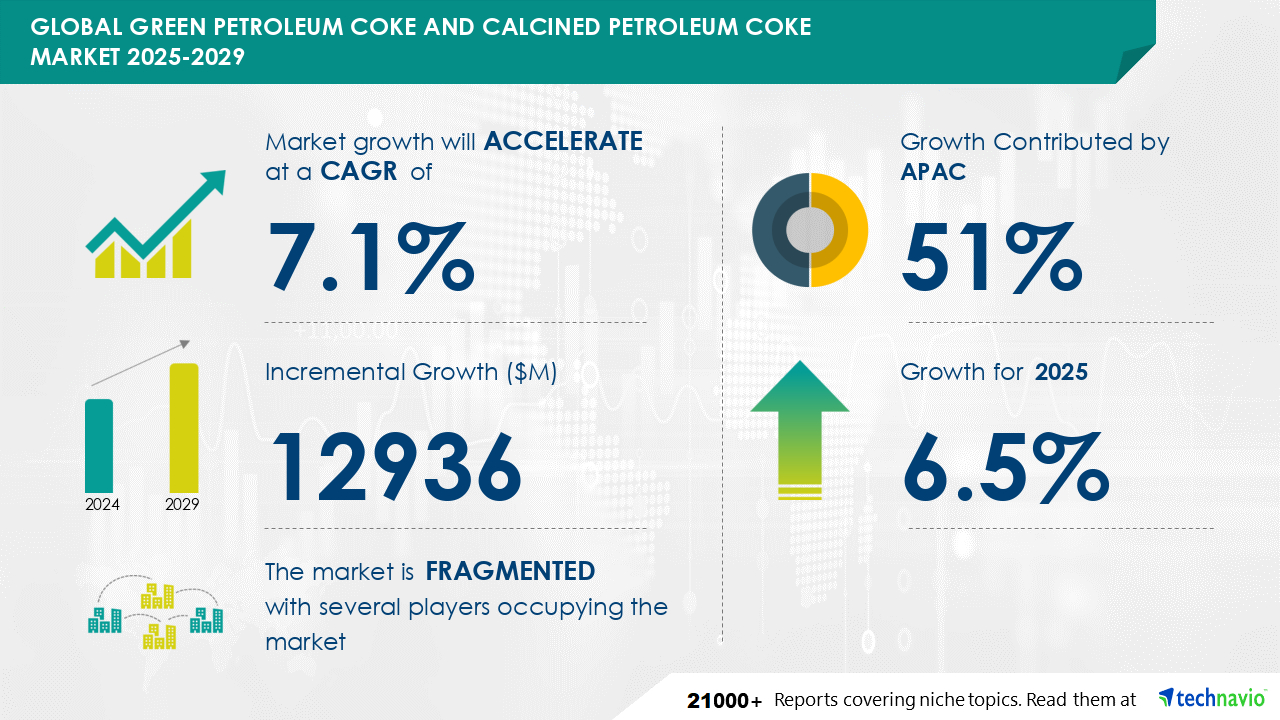

The Green Petroleum Coke And Calcined Petroleum Coke Market is expected to grow at a CAGR of 7.1% during 2024 and 2029. During this period, the market is also expected to show a growth of USD 12936 million. In the evolving oil and gas sector, automation is gaining significant traction due to technological advancements in machine learning, artificial intelligence, and robotics. Self-driving ore trucks and robotic drills are among the innovative machines revolutionizing oil refining processes, enhancing safety, efficiency, and production capacity. The oil industry's increasing reliance on automation and robotics will boost the value proposition for stakeholders and the industry as a whole. This automation trend is anticipated to stimulate the global production of crude oil, the primary feedstock for manufacturing green petroleum coke and calcined petroleum coke, throughout the forecast period.

Get more information on Green Petroleum Coke And Calcined Petroleum Coke Market by requesting a sample report

The market is segmented based on

According to Technavio, There are several factors that are causing the market to flourish during the forecast period, which are as follows:

However, the market also witnesses some limitations, which are as follows:

Rich Experience: 20+ years leading global market research, trusted insights across industries.

Unlock Business Potential with Technavio: Maximize ROI with Technavio's tailored market research: deep dives and actionable insights.

Your Guide to Market Success: Empower your business with Technavio's market research and future-proof your decisions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

208 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.1% |

|

Market growth 2025-2029 |

USD 12936 million |

|

Market structure |

fragmentation |

|

YoY growth 2024-2025(%) |

6.5 |

|

Key countries |

China, US, India, Germany, UK, Japan, Canada, France, South Korea, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Find out which segment is leading the market by accessing the free PDF report

The Green Petroleum Coke and Calcined Petroleum Coke market encompasses various aspects, including coke handling and bulk shipping, with a focus on quality assurance and process optimization for energy efficiency and cost reduction. Market analysis delves into technical aspects, competitive landscape, future outlook, and raw material sourcing. Production technology, application development, and end-user industries are key areas of interest. Consumer behavior, technological innovation, regulatory compliance, economic outlook, and demand forecasting are crucial factors influencing the market. Price volatility, global competition, trade relations, supply chain resilience, sustainability practices, environmental impact, carbon capture, waste reduction, circular economy, innovation strategies, and technological development are also significant elements shaping the market landscape. Investment opportunities are driven by these factors and ongoing regulatory requirements.

In the context of the global coal and consumable fuels market, Green Petroleum Coke and Calcined Petroleum Coke are essential by-products derived from petroleum refining processes. Manufacturers and providers of these coke types contribute significantly to the market's revenue. The market's expansion is driven by the escalating energy demand due to limited fossil fuel reserves and fuel price volatility. Government prioritization of energy security, with many countries being heavily reliant on coal imports, further bolsters market growth. Petroleum Coke quality, as determined by carbon and sulfur content, plays a crucial role in coke specifications and overall market dynamics.. Industries are leveraging the products belonging to the market for customer engagement, transactional notifications, and promotional offers.

Technavio Research

Jesse Maida

Media & Marketing Executive

US: +1 844 364 1100

UK: +44 203 893 3200

Email: media@technavio.com

Website: www.technavio.com/

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.