The Front End Of The Line Semiconductor Equipment Market is being driven by Growth of advanced consumer electronics industry

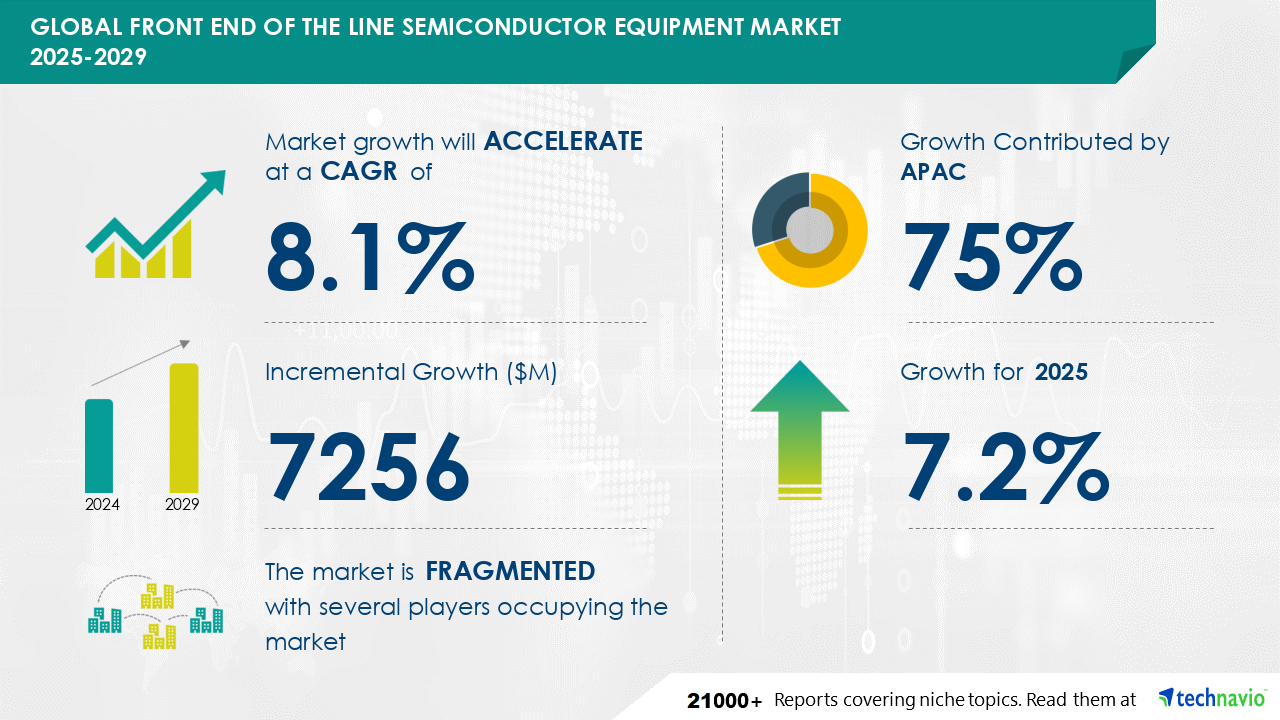

The Front End Of The Line Semiconductor Equipment Market is expected to grow at a CAGR of 8.1% during 2024 and 2029. During this period, the market is also expected to show a growth of USD 7256 million. The automotive industry is undergoing significant transformation, with a focus on electronics such as advanced driver assistance systems (ADAS), connected vehicles, and electric energy driving growth. Electronic content and associated systems will increasingly influence automobile purchasing decisions. Automakers integrate various types of semiconductor ICs into functions like airbag control, GPS, power doors and windows, ABS, car navigation and display, infotainment, and automated driving. The expanding automotive market, fueled by rising car production during the forecast period, will generate demand for semiconductor devices. Consequently, this demand will indirectly propel the growth of the front-end of the line semiconductor equipment market on a global scale.

Get more information on Front End Of The Line Semiconductor Equipment Market by requesting a sample report

The market is segmented based on

According to Technavio, There are several factors that are causing the market to flourish during the forecast period, which are as follows:

However, the market also witnesses some limitations, which are as follows:

Rich Experience: 20+ years leading global market research, trusted insights across industries.

Unlock Business Potential with Technavio: Maximize ROI with Technavio's tailored market research: deep dives and actionable insights.

Your Guide to Market Success: Empower your business with Technavio's market research and future-proof your decisions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

227 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.1% |

|

Market growth 2025-2029 |

USD 7256 million |

|

Market structure |

fragmentation |

|

YoY growth 2024-2025(%) |

7.2 |

|

Key countries |

Taiwan, US, China, Japan, South Korea, India, Canada, Mexico, UK, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Find out which segment is leading the market by accessing the free PDF report

The Front End of the Line (FEOL) semiconductor equipment market encompasses technologies such as wafer alignment systems, silicon wafer processing, and defect review systems. Key processes include lithographic process steps, reactive ion etching, deep ultraviolet lithography, extreme ultraviolet lithography, chemical vapor deposition, physical vapor deposition, and atomic layer deposition. Critical dimension metrology and overlay measurement ensure precision, while equipment downtime reduction, yield improvement methodologies, contamination mitigation, process variability reduction, and process simulation software optimize efficiency. Advanced process control, real-time process monitoring, and statistical process control maintain quality, and equipment qualification, process validation, failure analysis techniques, and cleanroom design specifications ensure reliability. Material compatibility testing is essential for maintaining optimal performance.

The Front End of the Line (FEOL) semiconductor equipment market encompasses manufacturers specializing in wafer cleaning systems, photolithography equipment, ion implantation technology, and thin film deposition. This sector falls under the broader global semiconductor materials and equipment market, which includes companies engaged in semiconductor materials production, fabrication, and wafer processing, as well as back-end manufacturing equipment (testing, assembly, and packaging). According to Technavio, the market size is determined by the revenue generated from sales of wafer processing, mask/reticle manufacturing, wafer manufacturing, fab facilities equipment, assembly and packaging, and test equipment. Market expansion will be fueled by escalating investments in semiconductor fabrication, with the establishment of new plants due to the surging demand for Integrated Circuits (ICs) worldwide.. Industries are leveraging the products belonging to the market for customer engagement, transactional notifications, and promotional offers.

Technavio Research

Jesse Maida

Media & Marketing Executive

US: +1 844 364 1100

UK: +44 203 893 3200

Email: media@technavio.com

Website: www.technavio.com/

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.