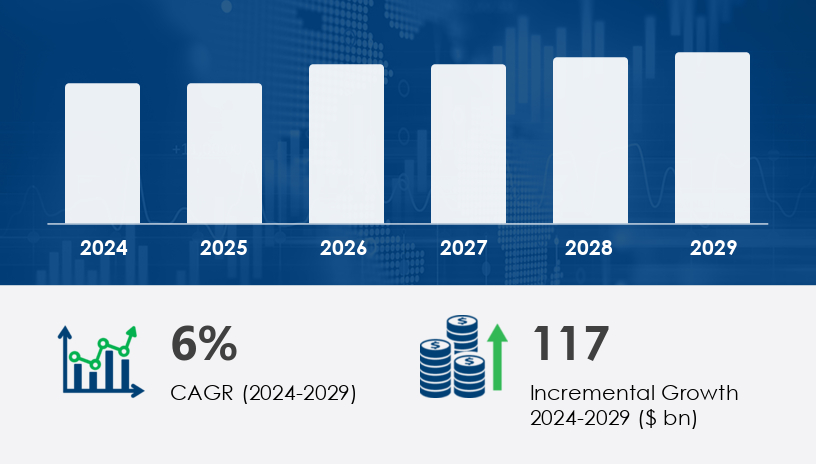

The Europe Aviation Market is set to witness significant expansion between 2025 and 2029, driven by increasing aircraft efficiency, sustainable innovations, and surging passenger volumes. With strategic advancements across airport infrastructure and digital transformation in operations, the region is cementing its place as a global aviation leader.According to market data, the Europe aviation market size is expected to increase by USD 117 billion during the forecast period, growing at a CAGR of 6% from 2024 to 2029. In 2024, the market showed robust performance and is forecast to reach new heights by 2029, reflecting dynamic demand across both passenger and freight services.For more details about the industry, get the PDF sample report for free

A primary driver fueling the Europe aviation market is the ongoing push for greater aircraft efficiency. Airlines and manufacturers are investing in technological upgrades, particularly in fleet renewal programs involving composite materials and advanced flight management systems. These innovations are aimed at reducing fuel consumption, enhancing performance, and minimizing environmental impact.

In line with global sustainability goals, the aviation sector in Europe must improve energy efficiency by over 3% annually by 2040. Key contributors include modern jet engines, AI-powered flight planning, and lightweight materials, which collectively optimize route planning, reduce emissions, and boost overall operational efficiency. Analyst insights emphasize the sector's focus on fleet optimization and flexible business models to adapt to fluctuating input costs, especially fuel prices.

A defining trend in the Europe aviation market is the adoption of RFID technology. This innovation is transforming both ground and flight operations by enabling real-time aircraft tracking, maintenance monitoring, and efficient baggage handling. By integrating RFID into manufacturing, route planning, and aircraft maintenance, airlines enhance airworthiness standards, reduce delays, and ensure on-time performance.

Furthermore, biometric authentication, smart airports, electric aircraft, and automated baggage systems are reshaping the passenger journey. Regulatory support and digital transformation in air traffic management are creating a robust infrastructure foundation. The use of AI in flight control, wearables for crew operations, and data-driven maintenance signifies a broader shift toward intelligent, eco-friendly aviation.

The Europe Aviation Market is undergoing a dynamic transformation fueled by the growth of commercial aircraft, business jets, and regional jets. As demand rebounds post-pandemic, airlines across the region are expanding fleets that include narrow-body aircraft, wide-body aircraft, and turboprop aircraft to service both short- and long-haul routes. The market is also benefiting from increased activity among low-cost carriers, charter flights, and private aviation. Supporting this ecosystem, airport infrastructure and runway systems are being upgraded to accommodate rising passenger volumes and newer freighter aircraft for expanding air cargo and air freight operations. Passenger airlines and cargo airlines alike are heavily investing in airport operations, baggage handling, and aviation logistics to meet efficiency and regulatory demands.

The Europe aviation market is segmented by:

Revenue Stream:

Passenger

Freight

Type:

Commercial Aircraft

Military Aircraft

General Aircraft

Component:

Aircraft

Maintenance, Repair, and Overhaul (MRO)

Ground Handling Services

Geography:

Europe

Among all segments, the passenger segment dominates the Europe aviation market, propelled by economic growth, rising disposable incomes, and increased air travel across the region. For example, in Q1 2023, the EU recorded 179 million passengers, a 56% increase over the same period in 2022.

The popularity of Europe as a tourist destination and the surge in intra-European travel has prompted fleet expansions by both full-service and low-cost carriers. According to analysts, the demand for aircraft acquisition and MRO services is directly linked to this passenger volume growth. Technologies like cabin comfort upgrades, in-flight entertainment, and biometric boarding are further elevating consumer expectations and contributing to segment momentum.

See What’s Inside: Access a Free Sample of Our In-Depth Market Research Report.

Unsurprisingly, Europe itself is the leading region within the Europe aviation market, maintaining the largest market share due to advanced infrastructure, a mature regulatory environment, and continuous innovation. The region carried approximately 820 million passengers in 2022, underscoring its strong position in global aviation.

Key countries such as Germany, France, and the UK are hubs for aircraft manufacturing, airline operations, and airport development. Analyst insights highlight how airport automation, fleet renewal, and aviation training in these markets drive demand for both aircraft and ancillary services. Strategic alliances like the Airbus and Rolls-Royce zero-emission engine project (2023) and the Lufthansa–Brussels Airlines merger (2024) are reshaping the regional competitive landscape.

One of the major challenges facing the Europe aviation market is the volatility in oil and gas prices, which directly impacts airline profitability. As fuel accounts for a significant portion of operational costs, any fluctuation in Brent crude oil, which was priced at USD 79.7 per barrel in January 2024, introduces uncertainty in pricing and strategic planning.This challenge necessitates flexible fuel procurement strategies, hedging, and investment in fuel-efficient technologies. Moreover, adapting to stringent environmental regulations and maintaining profitability amid fluctuating aviation fuel costs remains a balancing act for many operators.

Advancements in aircraft maintenance, MRO services, and aircraft engines continue to play a pivotal role in the performance and longevity of the aviation fleet. The integration of sophisticated avionics systems, upgraded cabin interiors, and next-gen in-flight entertainment solutions enhances the passenger experience, while aviation software and air traffic control improvements streamline scheduling and routing. As Europe pushes toward sustainability, the market sees growing interest in electric aircraft, hybrid aircraft, and sustainable aviation practices such as alternative aviation fuel and cleaner jet fuel usage. Meanwhile, innovation in drone technology and urban air mobility is expanding the region’s focus beyond traditional aviation, supported by robust aviation regulations, air traffic management, and airport security frameworks.

Workforce development is another major priority, with emphasis on flight training, pilot training, and aviation safety standards to ensure operational excellence. Investments in air navigation technologies and air traffic control systems aim to reduce delays and enhance safety across busy European airspaces. In addition to physical infrastructure, airport operations are embracing digital solutions for efficiency, including smart ground handling systems and automated baggage handling. The rise in aircraft leasing is enabling fleet modernization without major capital investment, while realistic flight simulators are being deployed for both commercial and private aviation training needs. As the region adapts to future challenges, the synergy between traditional air transport, regulatory advancement, and digital innovation is expected to keep the Europe Aviation Market on a sustained upward trajectory.

Companies in the Europe aviation market are pursuing strategic mergers, product launches, and sustainability collaborations to gain a competitive edge. Notable developments include:

February 2023: Airbus and Rolls-Royce announced a joint initiative to build zero-emission commercial aircraft engines.

April 2024: Ryanair launched Ryanair Sun, a long-haul subsidiary to expand beyond short-haul operations.

July 2024: Lufthansa Group merged with Brussels Airlines, creating a consolidated fleet of over 700 aircraft.

December 2025: The Boeing 737 MAX was re-certified by EASA for European airspace.

Major players like Air France KLM, BAE Systems, Dassault Aviation, Thales Group, and Honeywell are leveraging innovations in aircraft interiors, automation, flight control systems, and airport operations. Analysts suggest that companies focusing on AI, electric propulsion, and passenger experience innovations are likely to lead the market over the next decade.

The Europe Aviation Market is entering a transformative phase, driven by technological innovation, increasing passenger traffic, and sustainability imperatives. While fuel price volatility presents challenges, proactive investments in efficiency-enhancing technologies, smart infrastructure, and flexible fleet strategies are enabling market players to navigate headwinds effectively. With USD 117 billion in projected growth by 2029 and a steady 6% CAGR, Europe remains a focal point in global aviation advancement.

Executive Summary

Market Landscape

Market Sizing

Historic Market Size

Five Forces Analysis

Market Segmentation

6.1 Revenue Stream

6.1.1 Passenger

6.1.2 Freight

6.2 Type

6.2.1 Commercial Aircraft

6.2.2 Military Aircraft

6.2.3 General Aircraft

6.3 Component

6.3.1 Aircraft

6.3.2 MRO (Maintenance, Repair, Overhaul)

6.3.3 Ground Handling Services

6.4 Geography

6.4.1 Europe

Customer Landscape

Geographic Landscape

Drivers, Challenges, and Trends

Company Landscape

Company Analysis

Appendix

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.