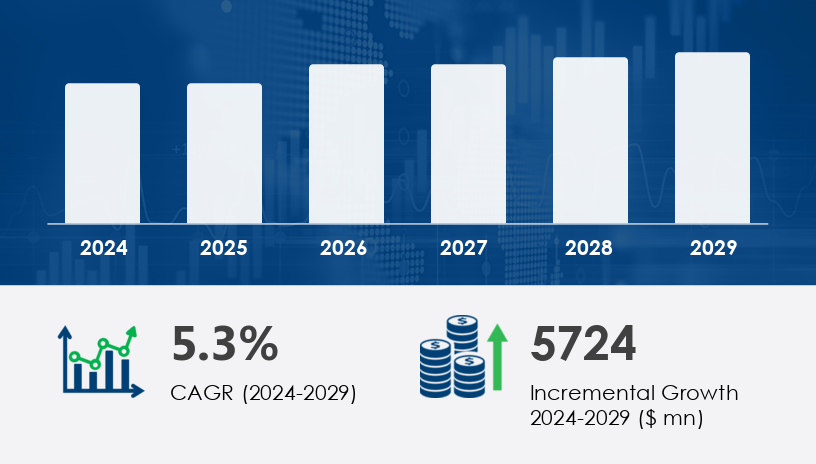

The global distribution transformers market is poised for significant growth, with projections indicating an increase of approximately USD 5.72 billion at a Compound Annual Growth Rate (CAGR) of 5.3% between 2024 and 2029. This expansion is driven by escalating power demands across residential, industrial, and commercial sectors, necessitating advanced and efficient distribution transformers to ensure reliable power supply and minimize energy losses. Additionally, the adoption of Distributed Energy Resource (DER) management systems is gaining momentum, further boosting the market's growth. These systems enable the integration of renewable energy sources into the power grid, thereby increasing the need for advanced and efficient distribution transformers. However, the market faces challenges due to the volatility of raw material prices, which can significantly impact the cost structure and profitability of distribution transformer manufacturers.

For more details about the industry, get the PDF sample report for free

The distribution transformers market is experiencing a transformative phase, characterized by technological advancements and a shift towards sustainable energy solutions. Key factors influencing this market include:

Urbanization and Industrialization: Rapid urban development and industrial growth are increasing electricity demand, thereby driving the need for efficient power distribution systems.

Integration of Renewable Energy: The growing adoption of renewable energy sources like solar and wind power requires grid modernization and smart transformers to manage the inherent variability of these energy sources.

Technological Innovations: Advances in transformer design, such as the development of smart transformers with monitoring capabilities, are enhancing grid reliability and efficiency.

Growth Drivers & Challenges:

Oil-filled transformers are favored for their higher efficiency and longer service life, making them suitable for high-capacity applications. However, concerns over environmental impact and maintenance requirements are steering some markets towards dry-type transformers, which are safer and require less maintenance.

Expert Insight:

"Oil-filled transformers continue to dominate in regions with high industrial activity due to their robustness and efficiency," notes an industry analyst. "However, the trend is shifting towards dry-type transformers in urban areas where safety and environmental concerns are paramount."

Mini Case Study:

In India, the Pradhan Mantri Sahaj Bijli Har Ghar Yojana (Saubhagya Scheme) aims to provide electricity to all households. The implementation strategy includes deploying both oil-filled and dry-type transformers to balance efficiency and safety in rural and urban areas, respectively.

Key Stats:

Oil-filled transformers account for a significant share of the market due to their efficiency and reliability.

Dry-type transformers are gaining popularity in urban settings due to safety and environmental considerations.

Get your free PDF sample report now for key industry insights and forecasts.

Growth Drivers & Challenges:

Power utilities require transformers for grid stability and load management, while industrial and commercial sectors demand high-capacity transformers to meet their energy needs. The challenge lies in balancing the supply to both sectors amidst fluctuating energy demands.

Expert Insight:

"The industrial sector's demand for high-capacity transformers is increasing as manufacturing activities expand," says a market expert. "Simultaneously, power utilities are focusing on upgrading aging infrastructure to maintain grid reliability."

Mini Case Study:

In Brazil, the expansion of the industrial sector has led to increased electricity consumption. To meet this demand, the government has invested in upgrading transformer infrastructure, focusing on both power utilities and industrial applications.

Key Stats:

The industrial sector is experiencing a surge in transformer demand due to increased manufacturing activities.

Power utilities are investing in infrastructure upgrades to ensure grid stability.

Growth Drivers & Challenges:

Smaller capacity transformers (below 500 kVA) are prevalent in residential areas, while medium to high-capacity transformers (500–2500 kVA and above 2500 kVA) cater to industrial and commercial needs. The challenge is to ensure the availability of transformers across all capacity ranges to meet diverse demands.

Expert Insight:

"There's a growing trend towards high-capacity transformers in industrial zones to support heavy machinery and equipment," observes an industry analyst. "Simultaneously, residential areas continue to require smaller capacity transformers for consistent power supply."

Mini Case Study:

In China, the rapid industrialization has increased the demand for high-capacity transformers. To address this, the government has initiated projects to manufacture and deploy transformers with capacities above 2500 kVA, particularly in industrial zones.

Key Stats:

High-capacity transformers are in demand in industrial zones to support heavy machinery.

Residential areas continue to require smaller capacity transformers for consistent power supply.

Market Research Overview

The Distribution Transformers Market is growing steadily due to rising demand for efficient and reliable power delivery across various sectors. Key product segments include the oil-filled transformer, dry-type transformer, liquid-immersed transformer, and gas-insulated transformer, all of which serve as vital components of modern power distribution transformer systems. Equipment such as the step-down stressor, pole-mounted transformer, and pad-mounted transformer are commonly deployed in residential and commercial applications. Technologies like the cast-resin transformer, amorphous core transformer, and silicon steel core have gained attention for their enhanced efficiency and performance. Essential structural elements include the transformer winding, high-voltage bushing, low-voltage bushing, and tap changer, each ensuring safe voltage regulation. Insulating materials such as transformer oil, mineral oil insulation, silicone oil insulation, and bio-based transformer oil contribute to operational longevity and environmental compliance. Cooling mechanisms like the cooling fan system, radiator cooling, forced-air cooling, and natural convection cooling are also key in preventing overheating and ensuring durability.

Opportunities:

Smart Grid Integration: The adoption of smart grid technologies presents opportunities for manufacturers to develop advanced transformers with monitoring and control capabilities.

Renewable Energy Integration: The increasing use of renewable energy sources necessitates the development of transformers capable of handling variable energy inputs.

Rural Electrification: Government initiatives aimed at providing electricity to rural areas create demand for distribution transformers.

Risks:

Raw Material Price Volatility: Fluctuations in the prices of materials like copper and steel can impact manufacturing costs.

Regulatory Compliance: Adhering to stringent environmental and safety regulations can increase operational costs.

Technological Obsolescence: Rapid technological advancements require continuous investment in research and development to stay competitive.

Unlock detailed market trends—download the complimentary PDF sample report.

The distribution transformers market is projected to reach USD 24.9 billion by 2029, growing at a CAGR of 6.1% from 2024 to 2029 . Key trends influencing this growth include:

Digitalization: The integration of digital technologies in transformers enables real-time monitoring and predictive maintenance.

Eco-Friendly Solutions: There is a growing emphasis on developing transformers with lower energy losses and improved environmental footprints.

Decentralized Energy Resources: The adoption of DERs necessitates the development of transformers capable of integrating with decentralized energy sources.

Expert Prediction:

"By 2029, we anticipate a significant shift towards smart, eco-friendly transformers equipped with digital capabilities to meet the evolving demands of modern power grids," predicts a leading industry expert.

Research Analysis Overview

Analytical insights into the distribution transformers market highlight technological advancements and emerging applications across diverse power systems. Innovations in transformer enclosure and weatherproof transformer designs enhance equipment resilience in extreme environments. Critical infrastructure like the substation transformer and compact distribution transformer is being optimized for both space-saving and high-performance applications. Emphasis on energy conservation has driven the rise of the energy-efficient transformer, low-loss transformer, and smart grid transformer, aligning with modern grid requirements. Voltage regulation technologies including the voltage regulator and load tap changer are being integrated for more dynamic power control. Advanced diagnostic tools like the transformer monitoring system and dissolved gas analysis are improving predictive maintenance and reducing downtime. Enhanced insulation materials such as transformer insulation, epoxy resin insulation, and Nomex insulation ensure thermal stability and safety. Market segmentation also includes the utility transformer, industrial transformer, commercial transformer, and residential transformer, each tailored to specific load demands. With the global push for renewables, renewable energy transformer, wind farm transformer, and solar plant transformer are emerging as high-growth categories within the sector.

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.