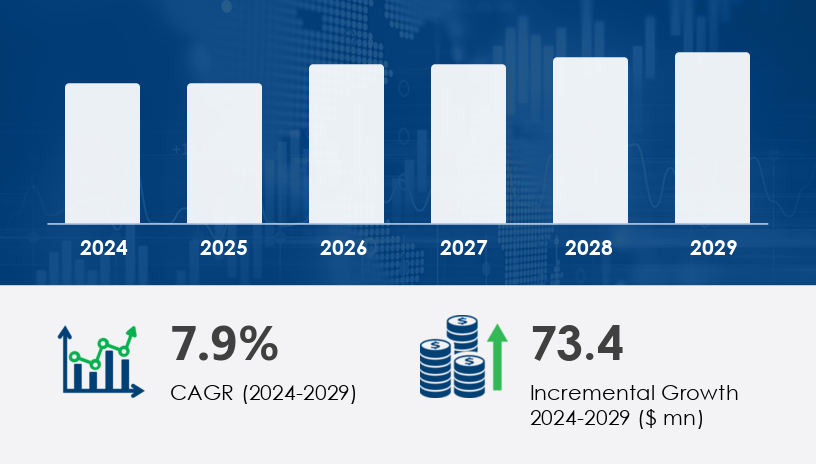

The digit joint implants market is poised for significant expansion, with projections indicating an increase of USD 73.4 million at a compound annual growth rate (CAGR) of 7.9% between 2024 and 2029. This growth is primarily driven by the rising prevalence of osteoarthritis and the increasing adoption of biodegradable implant materials. However, the market faces challenges such as high costs, regulatory hurdles, and supply chain inconsistencies.For more details about the industry, get the PDF sample report for free

A primary driver for the Digit Joint Implants Market is the rising prevalence of osteoarthritis (OA), a degenerative joint disease that affects over 10% of the global population. In the U.S. alone, more than 30 million adults suffer from OA, as per the Centers for Disease Control and Prevention (CDC). This condition severely impacts joint mobility and functionality, prompting a high demand for effective surgical interventions like digit joint implants.

Technological advancements, especially in 3D printing, now allow for customized implants tailored to each patient’s anatomy, enhancing implant stability and improving clinical outcomes. Analyst commentary suggests that implant design and patient-centric approaches will be crucial in enhancing post-surgical satisfaction and sustaining market momentum.

One of the most transformative trends in the market is the growing preference for biodegradable digit joint implants. These implants, composed of materials like polyglycolic acid (PGA) and polylactic acid (PLA), offer enhanced biocompatibility and reduce the need for revision surgeries by disintegrating over time and promoting bone tissue regrowth.

For instance, RegJoint, a biodegradable implant designed for finger and toe joints, has shown success in alleviating pain and improving joint mobility in OA and RA patients. Analysts note that this trend aligns with the industry's broader shift toward patient-friendly solutions and outpatient joint replacement procedures, which contribute to higher patient satisfaction and better long-term outcomes.

The Digit Joint Implants Market is experiencing significant growth, driven by rising cases of osteoarthritis and rheumatoid arthritis affecting the fingers, toes, and small joints. Common implant types include MCP joint implants, PIP joint implants, MTP joint implants, and trapeziometacarpal implants, as well as specialized products like toe implants, metacarpal joint implants, and metatarsal joint implants. These orthopedic digit implants are used in arthroplasty implants procedures to restore joint mobility, improve hand and foot function, and relieve chronic pain. Innovations such as 3D printed implants, custom digit implants, and computer-aided implants are enhancing outcomes through tailored fits and faster recovery times. The demand for minimally invasive implants that support bone preservation and articular cartilage restoration is on the rise, especially for conditions like hallux rigidus.

The Digit Joint Implants Market is segmented by:

Product

MCP and PIP

Trapeziometacarpal

Toe implants

Others

Type

Foot

Hands

Material

Titanium

Polymers

Nitinol

Ceramics

Geography

North America

Europe

APAC

South America

Rest of World (ROW)

Among the product segments, the MCP and PIP segment leads in terms of both revenue and growth. This segment was valued at USD 64.60 million in 2019 and has seen a steady increase over the forecast period. Innovations in biocompatible materials such as titanium alloys, ceramics, and pyrocarbon have enhanced implant durability and patient outcomes.

Furthermore, robotic surgery and minimally invasive techniques have enabled faster patient recovery and higher satisfaction rates. Analysts emphasize that the combination of regenerative medicine, insurance expansion, and customized 3D-printed implants is expected to further solidify this segment's dominance through 2029.

North America accounts for 46% of the global market share and is expected to maintain its dominance through 2029. The region benefits from a robust healthcare infrastructure, extensive insurance coverage, and high adoption of minimally invasive surgical procedures. The U.S. in particular leads the market, supported by high healthcare spending, widespread use of advanced implants, and an aging population highly prone to OA and RA.

Advanced technologies like 3D printing and robotic-assisted surgeries are widely adopted in the region, enabling custom implant fabrication and faster patient rehabilitation. Analysts observe that the presence of ambulatory surgery centers and regulatory support for outpatient procedures is helping improve accessibility and cost-efficiency, making North America a cornerstone of global market growth.

Despite strong growth potential, the market faces a significant challenge: the high cost of digit joint implants and associated surgical procedures. These costs can increase by 130–150% throughout the value chain. Biodegradable and absorbable implants, while clinically advantageous, are typically more expensive than traditional metallic alternatives.

This price barrier can limit accessibility, especially in lower-income demographics and emerging markets. Additionally, stringent regulatory approvals and supply chain inconsistencies further complicate market entry and timely product delivery. Analysts suggest that cost-reduction strategies and supply chain optimization will be critical for manufacturers seeking long-term success in this competitive landscape.

Material advancements are central to the performance of digit joint implants. Key implant materials include pyrocarbon implants, titanium implants, nitinol implants, cobalt chrome implants, polyethylene implants, biodegradable implants, and silicone implants, all selected for their biocompatible properties and durable construction. Devices such as intramedullary digit implants, flexible intramedullary implants, hemi phalangeal implants, and Morse taper implants offer enhanced anatomical compatibility, especially in finger joint implants and toe HemiCAP implants. These joint replacement implants help achieve a balance between mechanical strength and flexibility, critical for long-term success in active individuals. Additionally, custom prosthetic digits and stable construction implants are playing an increasingly important role in both trauma care and degenerative joint disease management

Growing interest in joint restoration implants and biomechanics implants is reshaping clinical approaches to hand joint implants and foot joint implants. Surgeons now seek advanced biomaterials and one-piece implants that reduce failure risks and improve functional restoration. Devices aimed at the scaphoid bone, digit, and phalangeal joints are being refined with joint mobility implants and osteointegrative properties for long-term success. Technologies like computer-aided implants and custom digit implants are helping deliver precision treatment in orthopedic procedures. Moreover, the integration of smart surgical planning tools is contributing to better implant alignment and faster post-operative rehabilitation, especially in patients requiring joint replacement implants for degenerative or traumatic conditions.

Leading companies in the Digit Joint Implants Market are prioritizing technological innovation, particularly in the areas of 3D printing, biocompatible materials, and computer-assisted surgeries. Efforts are also underway to improve remote patient monitoring, enhance pre-operative planning, and leverage AI and big data to support personalized medicine.

For example, clinical trials led by the University of Hong Kong and the Productivity Council are exploring 3D-printed plastic models with metal integration for finger joint implants. These efforts aim to reduce implant import dependency and promote cost-effective local production.

Furthermore, digital health technologies, including image-guided surgeries and long-term follow-up systems, are enabling better outcomes and infection control. Analyst insights underscore the need for companies to focus on regulatory compliance, material innovation, and minimally invasive techniques to maintain their competitive edge.

Executive Summary

Market Landscape

Market Sizing

Historic Market Size

Five Forces Analysis

Market Segmentation

6.1 Product

6.1.1 MCP and PIP

6.1.2 Trapeziometacarpal

6.1.3 Toe Implants

6.1.4 Others

6.2 Type

6.2.1 Hands

6.2.2 Foot

6.3 Material

6.3.1 Titanium

6.3.2 Polymers

6.3.3 Nitinol

6.3.4 Ceramics

6.4 Geography

6.4.1 North America

6.4.2 Europe

6.4.3 APAC

6.4.4 South America

6.4.5 Middle East and Africa

6.4.6 Rest of World (ROW)

Customer Landscape

Geographic Landscape

Drivers, Challenges, and Trends

Company Landscape

Company Analysis

Appendix

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.