The Data Center Server Market is being driven by Investments in scaling up in-house data centers

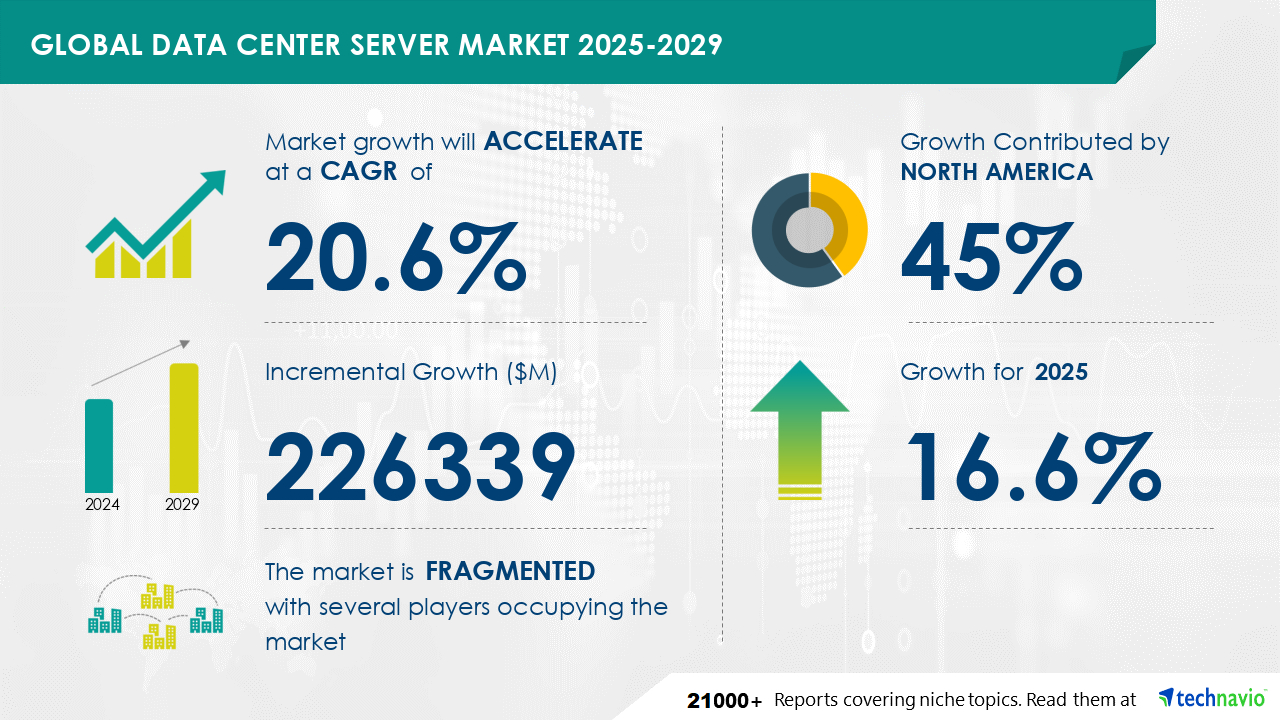

The Data Center Server Market is expected to grow at a CAGR of 20.6% during 2024 and 2029. During this period, the market is also expected to show a growth of USD 226339 million. Data centers face escalating power demands as a result of the expanding adoption of cloud computing, advanced AI, machine learning, and IoT workloads on servers. With the inability to decrease their server inventory, data center operators seek solutions to optimize server utilization and subsequently decrease energy consumption. By implementing server disaggregation, data centers can enhance server utilization rates, reducing the need for a larger number of servers to process existing workloads and consequently lowering power consumption. This approach enables data centers to efficiently manage their resources and maintain a competitive edge in the market.

Get more information on Data Center Server Market by requesting a sample report

The market is segmented based on

According to Technavio, There are several factors that are causing the market to flourish during the forecast period, which are as follows:

However, the market also witnesses some limitations, which are as follows:

Rich Experience: 20+ years leading global market research, trusted insights across industries.

Unlock Business Potential with Technavio: Maximize ROI with Technavio's tailored market research: deep dives and actionable insights.

Your Guide to Market Success: Empower your business with Technavio's market research and future-proof your decisions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

226 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 20.6% |

|

Market growth 2025-2029 |

USD 226339 million |

|

Market structure |

fragmentation |

|

YoY growth 2024-2025(%) |

16.6 |

|

Key countries |

US, China, India, Canada, Germany, Japan, UK, France, Brazil, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Find out which segment is leading the market by accessing the free PDF report

The Data Center Server Market encompasses advanced technologies like blade server technology, which optimizes server room design, and ensures high data center uptime through server provisioning and maintenance. Network latency reduction is achieved via server consolidation, storage virtualization, and network topology design. IT infrastructure costs are minimized through server deployment automation, server architecture design, and server resource allocation. Server security and data center efficiency are enhanced with server monitoring tools, network security appliances, server patching strategies, and virtual machine optimization. Data center footprint is reduced through server consolidation and storage virtualization. Server upgrade cycles are managed effectively with IT infrastructure resilience and server architecture design. Data center airflow is optimized for cooling efficiency, and server patching strategies ensure minimal downtime. Storage performance metrics provide insights into server resource allocation and server architecture design.

The communications equipment market encompasses the revenue generated from the sale of telecommunication, broadcasting, and communication infrastructure equipment. This market is driven by the expanding data center sector, with hyperscalers investing heavily in the construction of new facilities and the expansion of existing ones. Server virtualization, rack space optimization, power usage effectiveness, and thermal management systems are key trends in the data center server market, contributing to its growth. Technavio's market analysis also includes the telecom equipment market within the communications equipment market scope. The market's growth is further fueled by the increasing demand for advanced communication solutions to support business operations and digital transformation initiatives.. Industries are leveraging the products belonging to the market for customer engagement, transactional notifications, and promotional offers.

Technavio Research

Jesse Maida

Media & Marketing Executive

US: +1 844 364 1100

UK: +44 203 893 3200

Email: media@technavio.com

Website: www.technavio.com/

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.