The Data Center Power Market is being driven by Increasing investments in data centers

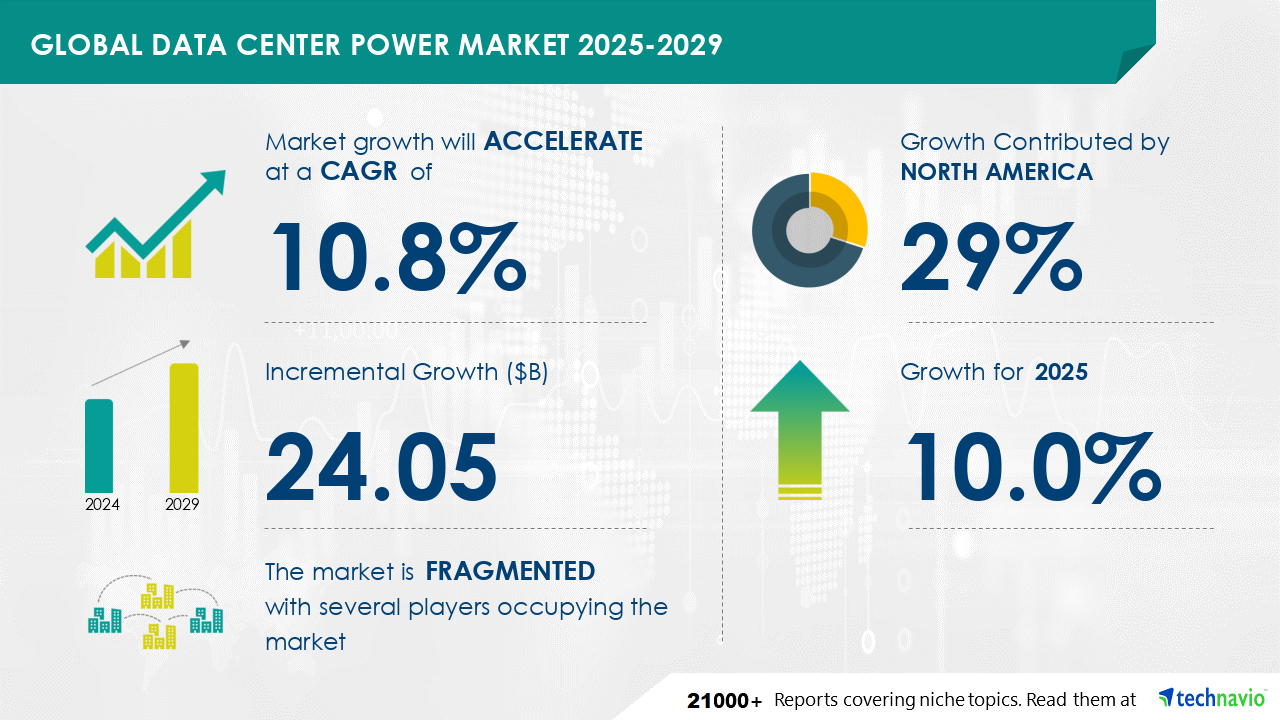

The Data Center Power Market is expected to grow at a CAGR of 10.8% during 2024 and 2029. During this period, the market is also expected to show a growth of USD 24.05 billion. In the realm of data center technology, High Performance Computing (HPC) represents a business solution designed to enhance computational capabilities and efficiency. HPC systems consist of interconnected clusters, ranging from 16 to 64 nodes, engineered to execute complex algorithms and simulations. These systems cater primarily to scientific and engineering applications, delivering superior performance compared to general-purpose computers. The performance metric for HPC systems is measured in Floating-Point Operations Per Second (FLOPS), as opposed to Million Instructions Per Second (MIPS). By employing HPC systems, businesses can expedite the resolution of recurring problems and intricate operations, including physical simulations, weather forecasting, quantum mechanics, and molecular modeling. These systems enable organizations to achieve significant time and cost savings, making them an indispensable asset in today's data-driven business landscape.

Get more information on Data Center Power Market by requesting a sample report

The market is segmented based on

According to Technavio, There are several factors that are causing the market to flourish during the forecast period, which are as follows:

However, the market also witnesses some limitations, which are as follows:

Rich Experience: 20+ years leading global market research, trusted insights across industries.

Unlock Business Potential with Technavio: Maximize ROI with Technavio's tailored market research: deep dives and actionable insights.

Your Guide to Market Success: Empower your business with Technavio's market research and future-proof your decisions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

227 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.8% |

|

Market growth 2025-2029 |

USD 24.05 billion |

|

Market structure |

fragmentation |

|

YoY growth 2024-2025(%) |

10.0 |

|

Key countries |

US, China, Australia, Canada, UK, Japan, France, Germany, India, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Find out which segment is leading the market by accessing the free PDF report

In the Data Center Power Market, optimizing power density and designing efficient cooling systems are key focuses. Energy consumption analysis and capacity expansion planning require careful consideration of power infrastructure design and system redundancy. Load management strategies, risk assessment methods, and power system monitoring ensure operational resilience. Preventive maintenance and infrastructure upgrades reduce environmental impact and ensure regulatory compliance. High-density computing necessitates advanced power system architecture and thermal modeling techniques. Lifecycle cost analysis and system uptime are essential for effective facility management. Electrical safety, infrastructure security, and power consumption trends are also critical factors in power system design. Capacity management and environmental impact are ongoing concerns, while regulatory compliance and system uptime ensure business continuity. Cooling technology selection, energy audit procedures, and power system upgrades are important steps in optimizing data center efficiency.

The Data Center Market, a significant segment of the Internet Services and Infrastructure industry, encompasses companies providing power usage effectiveness solutions, Uninterruptible Power Supply (UPS) systems, and precision cooling systems. Power Usage Effectiveness (PUE) is a critical energy efficiency metric that measures the ratio of total facility power to IT equipment power. UPS systems ensure uninterrupted power supply, preventing downtime and data loss. Precision cooling systems optimize cooling efficiency, reducing energy consumption and enhancing overall data center performance. These technologies contribute to the market's growth, prioritizing energy efficiency and reliability.. Industries are leveraging the products belonging to the market for customer engagement, transactional notifications, and promotional offers.

Technavio Research

Jesse Maida

Media & Marketing Executive

US: +1 844 364 1100

UK: +44 203 893 3200

Email: media@technavio.com

Website: www.technavio.com/

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.