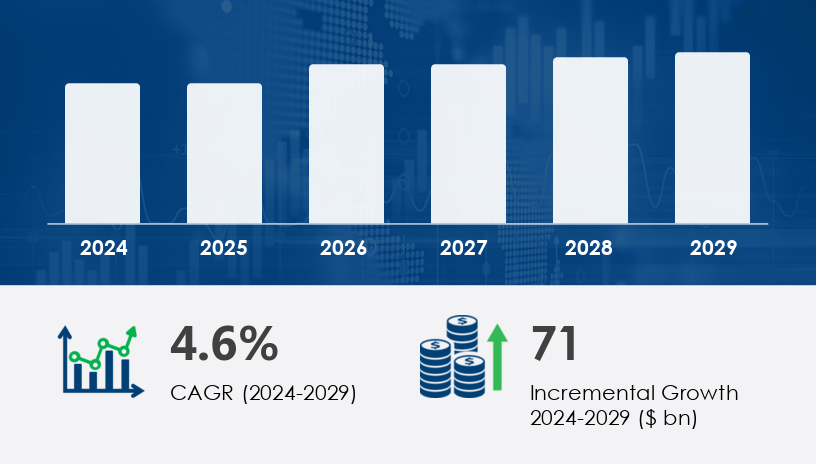

The global confectionery market is poised for significant growth between 2025 and 2029, with a projected increase of USD 71 billion at a compound annual growth rate (CAGR) of 4.6%. This expansion is driven by evolving consumer preferences, the growth of e-commerce retailing, and a heightened focus on health-conscious indulgence. In this comprehensive guide, we delve into the key market segments—distribution channels, product types, age demographics, and pricing strategies—to provide actionable insights for industry stakeholders.

For more details about the industry, get the PDF sample report for free

The confectionery market is experiencing dynamic shifts as it adapts to changing consumer behaviors and economic factors. The industry's growth is underpinned by several key drivers, including:

E-commerce Expansion: The rise of online retailing offers consumers greater convenience and access to a broader range of products.

Health-Conscious Choices: An increasing demand for healthier alternatives is influencing product formulations and offerings.

Premiumization Trend: Consumers are gravitating towards high-quality, artisanal products, willing to pay a premium for superior taste and ingredients.

However, the market also faces challenges such as:

Supply Chain Disruptions: Issues like restricted public mobility and workforce shortages can impact production and distribution.

Rising Raw Material Costs: Fluctuations in the prices of key ingredients like cocoa and sugar affect profit margins.

Regulatory Pressures: Governments are implementing guidelines to address health concerns related to sugar consumption.

| Segment | Key Drivers | Challenges |

|---|---|---|

| Distribution | E-commerce growth, convenience | Supply chain complexities |

| Product Type | Health trends, premiumization | Ingredient sourcing issues |

| Age Demographics | Tailored offerings for all age groups | Changing dietary habits |

| Pricing Strategy | Value for money, luxury indulgence | Economic fluctuations |

Growth Drivers & Challenges: The offline segment remains robust, with hypermarkets and convenience stores playing pivotal roles. However, the online channel is rapidly gaining traction, driven by the convenience of home delivery and a wider product selection. Challenges include supply chain disruptions and the need for retailers to adapt to digital platforms.

Expert Insight: "The convergence of offline and online channels is reshaping the retail landscape, requiring businesses to adopt an omnichannel approach to meet consumer expectations."

Mini Case Study: A leading confectionery brand expanded its online presence, resulting in a 30% increase in sales within the first quarter, demonstrating the efficacy of digital transformation.

See What’s Inside: Access a Free Sample of Our In-Depth Market Research Report.

Growth Drivers & Challenges: Chocolate remains the dominant category, with innovations like dark premium chocolates and sugar-free variants catering to health-conscious consumers. Sugar confectionery and gums are also witnessing growth, particularly among younger demographics. The challenge lies in sourcing quality ingredients amid rising costs.

Expert Insight: "Product innovation is key to staying competitive; companies must balance indulgence with health-conscious offerings to appeal to a broader audience."

Mini Case Study: A major confectionery manufacturer introduced a line of organic, sugar-free chocolates, leading to a 25% increase in market share within six months.

Growth Drivers & Challenges: Tailoring products to specific age groups enhances consumer engagement. For instance, sugar-free and functional confectioneries appeal to older demographics, while vibrant, novelty items attract children. The challenge is to continuously innovate to meet the diverse preferences of each age group.

Expert Insight: "Understanding the unique preferences of each age group allows for more targeted marketing and product development strategies."

Mini Case Study: A confectionery brand launched a line of vitamin-infused gummies targeted at children, resulting in a 40% increase in sales among the youth segment.

Growth Drivers & Challenges: The market is segmented into economy, mid-range, and luxury categories. Economic fluctuations influence consumer spending habits, while the demand for premium products is driven by consumers seeking quality and indulgence. Balancing cost and quality remains a challenge.

Expert Insight: "The premiumization trend is evident, with consumers willing to pay more for high-quality, artisanal products that offer a unique experience."

Mini Case Study: A luxury chocolate brand maintained its market position by focusing on quality and exclusivity, even as mass-market products faced declining sales due to rising cocoa prices.

Emerging Markets: Expanding into regions with growing middle-class populations presents significant growth potential.

Health-Conscious Products: Developing sugar-free, organic, and functional confectioneries can cater to the increasing demand for healthier options.

E-commerce Expansion: Strengthening online retail channels can enhance accessibility and reach a broader consumer base.

Supply Chain Disruptions: Ongoing challenges in sourcing raw materials can impact production timelines and costs.

Regulatory Changes: New regulations aimed at reducing sugar consumption may affect product formulations and marketing strategies.

Economic Instability: Fluctuations in the global economy can influence consumer spending behavior and demand for confectionery products.

The Confectionery Market is undergoing a significant transformation driven by evolving consumer preferences, with a strong shift toward healthier and more ethical options. Products such as organic chocolate, sugar-free gummies, artisanal candies, and dark chocolate are becoming increasingly popular among health-conscious and ethically minded consumers. There's a growing demand for vegan chocolates, gluten-free sweets, and premium chocolates, reflecting a broader interest in clean eating and indulgence without compromise. The rise of functional confectionery and the inclusion of natural ingredients are also influencing purchase decisions, particularly for products like chocolate bars, chewing gum, hard candies, and toffees. Trends such as marshmallows, lollipops, jelly beans, and fruit chews are being reimagined with reduced sugar, Fairtrade cocoa, and non-GMO ingredients. Additionally, innovations in plant-based sweets, exotic flavors, and health-conscious snacks reflect the market’s responsiveness to changing dietary needs and values.

The confectionery market is expected to grow by USD 71 billion from 2024 to 2029, expanding at a CAGR of 4.6%. This growth is driven by:

Product Innovation: Continuous development of new flavors and healthier alternatives.

Digital Transformation: Increased adoption of e-commerce platforms for sales and marketing.

Consumer Trends: A shift towards premium, artisanal products and health-conscious choices.

Expert Prediction: "The next five years will see a convergence of health and indulgence in the confectionery sector, with brands that successfully integrate these elements leading the market."

For Distribution Channels:

Omnichannel Strategy: Integrate offline and online platforms to provide a seamless shopping experience.

Supply Chain Optimization: Invest in technology to enhance logistics and reduce disruptions.

Retail Partnerships: Collaborate with retailers to expand product reach and visibility.

For Product Development:

Health-Focused Offerings: Develop sugar-free, organic, and functional products to meet health-conscious demands.

Innovative Flavors: Experiment with unique flavor combinations to attract adventurous consumers.

Request Your Free Report Sample – Uncover Key Trends & Opportunities Today

Analytical insights into the confectionery market reveal an increasing focus on enhancing value propositions through ingredients and presentation. Products are now being developed with superfood ingredients to deliver added nutritional benefits, particularly in formats like snack bars, fortified gummies, and low-calorie sweets. Strategic use of e-commerce platforms and social media marketing is helping brands reach younger and digitally-savvy demographics. Packaging trends like innovative packaging, attractive jars, resalable packaging, and family-sized packs are improving product appeal and convenience. The emphasis on sustainable sourcing, clean label, and natural sweeteners supports environmentally and health-conscious consumers. High-end offerings such as gourmet chocolates, seasonal variants, and sugar-free chocolates cater to both premium and niche markets. Further, aspects such as cocoa content, bean-to-bar processes, and medicated confectionery demonstrate the growing importance of transparency, quality, and functionality in product development and consumer engagement.

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.