The Computational Fluid Dynamics (CFD) Market is being driven by Growing need for reduction in product design time and cost

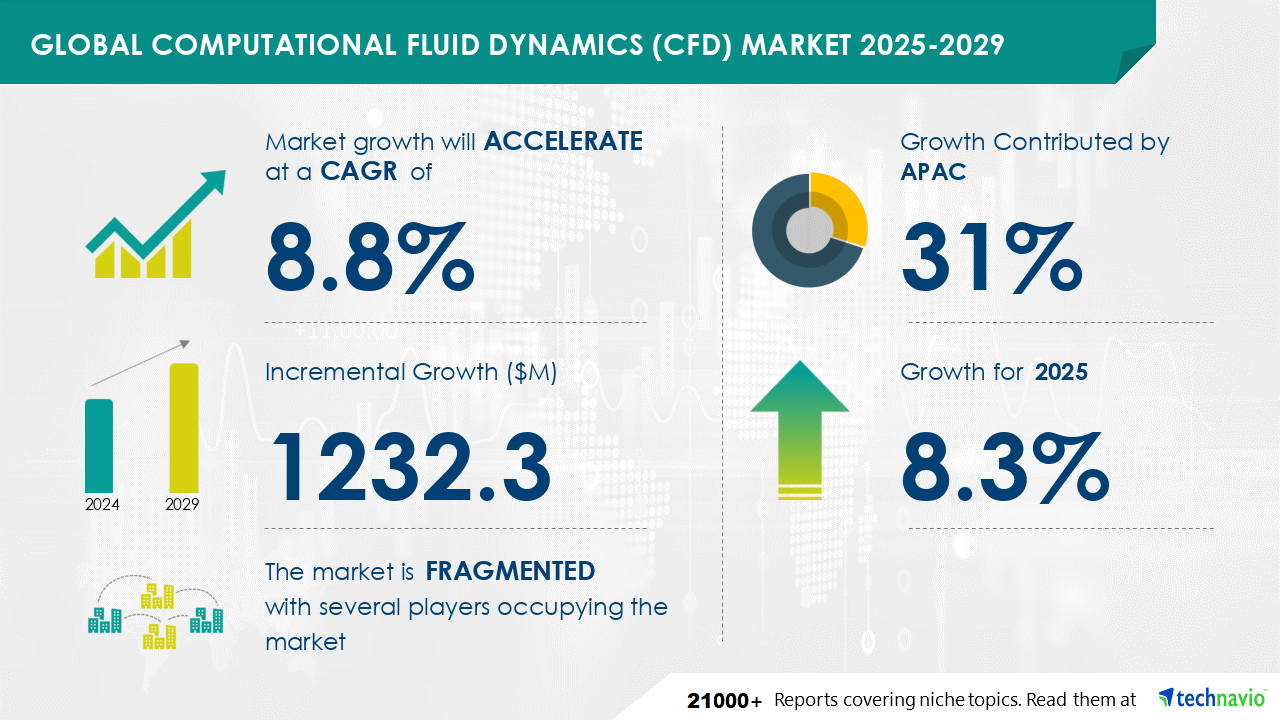

The Computational Fluid Dynamics (CFD) Market is expected to grow at a CAGR of 8.8% during 2024 and 2029. During this period, the market is also expected to show a growth of USD 1232.3 million. In today's business landscape, the increasing demand for digital transformation, connectivity, and user-friendly solutions has significantly expanded the market share of Computational Fluid Dynamics (CFD) in developing economies. Vendors are responding to this trend by developing advanced, cloud-based Product Lifecycle Management (PLM) offerings, enabling users to access feature-rich CFD software without the need for installation, IT system configurations, license activations, or hardware setups. Cloud solutions offer a streamlined experience, providing a guided workflow and a smooth learning curve for new adopters, ensuring a quick and efficient onboarding process. The elimination of upfront costs and the ability to scale usage as needed further enhance the appeal of cloud-based CFD services in the corporate world.

Get more information on Computational Fluid Dynamics (CFD) Market by requesting a sample report

The market is segmented based on

According to Technavio, There are several factors that are causing the market to flourish during the forecast period, which are as follows:

However, the market also witnesses some limitations, which are as follows:

Rich Experience: 20+ years leading global market research, trusted insights across industries.

Unlock Business Potential with Technavio: Maximize ROI with Technavio's tailored market research: deep dives and actionable insights.

Your Guide to Market Success: Empower your business with Technavio's market research and future-proof your decisions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

206 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.8% |

|

Market growth 2025-2029 |

USD 1232.3 million |

|

Market structure |

fragmentation |

|

YoY growth 2024-2025(%) |

8.3 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, Rest of World (ROW), US, China, Germany, UK, India, Canada, South Korea, France, Japan, Italy, Brazil, and USA |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Find out which segment is leading the market by accessing the free PDF report

The Computational Fluid Dynamics (CFD) market encompasses various solutions, including CFD simulation software, flow visualization tools, and associated technologies. Key components include mesh quality assessment, grid independence studies, numerical stability analysis, and accuracy assessments. Model calibration, CFD code development, and case study applications are also crucial. Benchmark problems and validation datasets are utilized for uncertainty quantification, sensitivity analysis, design optimization, and experimental design. Data acquisition systems, flow measurement techniques, temperature measurement, and pressure sensors are essential for data collection. Data analysis techniques, statistical methods, and visualization techniques are used for data interpretation, while problem definition, model selection, and simulation setup complete the CFD process.

In the dynamic and expansive realm of the global IT software industry, the Computational Fluid Dynamics (CFD) market occupies a significant niche. This sector caters to organizations specializing in CFD simulation software, which employs advanced techniques such as mesh generation, finite volume method, and the solution of Navier-Stokes equations, coupled with sophisticated turbulence modeling and precise boundary condition implementation. These elements enable the analysis and optimization of fluid flow and related phenomena, contributing to the development of efficient systems in industries like automotive, aerospace, and energy. The CFD market size is determined by the consolidated revenue generated by these specialized software providers, as calculated by Technavio within the broader context of the global IT systems software market.. Industries are leveraging the products belonging to the market for customer engagement, transactional notifications, and promotional offers.

Technavio Research

Jesse Maida

Media & Marketing Executive

US: +1 844 364 1100

UK: +44 203 893 3200

Email: media@technavio.com

Website: www.technavio.com/

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.

Market 2025-2029")