The Bunker Fuel Market is being driven by Increasing naval expenditure

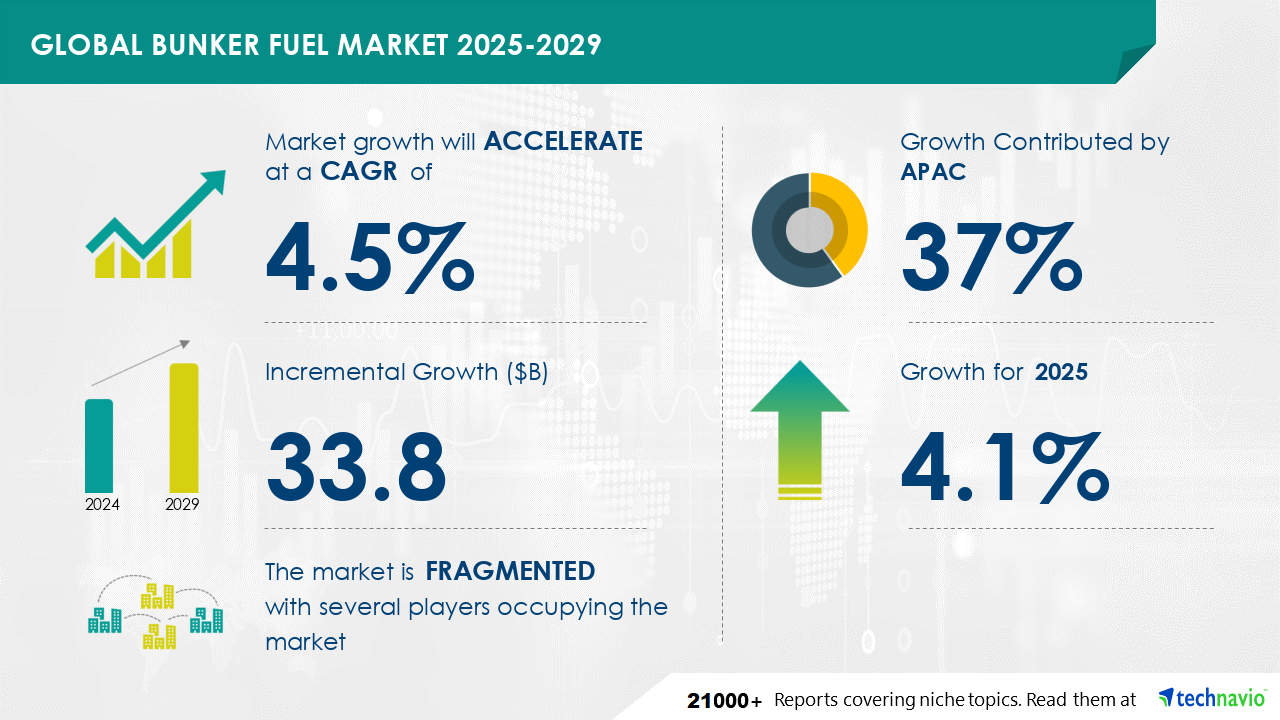

The Bunker Fuel Market is expected to grow at a CAGR of 4.5% during 2024 and 2029. During this period, the market is also expected to show a growth of USD 33.8 billion. The maritime industry is witnessing a notable shift towards the use of liquefied natural gas (LNG) as an alternative fuel for ocean-going vessels. LNG offers several advantages, including its ability to reduce greenhouse gas (GHG) emissions, as it is odorless, non-toxic, and non-corrosive. Moreover, LNG evaporates quickly upon exposure to air, leaving no residue behind. Despite oil-based fuels being the primary choice for marine transportation, LNG is gaining prominence due to the escalating number of LNG projects in execution and planning. Compliance with current emission norms is a significant factor driving the adoption of LNG as a fuel, as it can substantially decrease sulfur oxides (SOx), nitrogen oxides (NOx), and carbon dioxide (CO2) emissions.

Get more information on Bunker Fuel Market by requesting a sample report

The market is segmented based on

According to Technavio, There are several factors that are causing the market to flourish during the forecast period, which are as follows:

However, the market also witnesses some limitations, which are as follows:

Rich Experience: 20+ years leading global market research, trusted insights across industries.

Unlock Business Potential with Technavio: Maximize ROI with Technavio's tailored market research: deep dives and actionable insights.

Your Guide to Market Success: Empower your business with Technavio's market research and future-proof your decisions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

230 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2025-2029 |

USD 33.8 billion |

|

Market structure |

fragmentation |

|

YoY growth 2024-2025(%) |

4.1 |

|

Key countries |

US, China, Singapore, Germany, UK, UAE, The Netherlands, Japan, France, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Find out which segment is leading the market by accessing the free PDF report

The Bunker Fuel Market encompasses the production, distribution, trading, and consumption of heavy fuel oils used for maritime transportation. Key specifications include cetane number, flash point, pour point, water content, sulfur content, and calorific value, which are assessed through fuel oil analysis and adherence to fuel oil specifications and standards. Certification, bunker delivery notes, and quantity measurement are crucial aspects of bunkering contracts and agreements, which may lead to disputes. Fuel oil prices, trends, and supply-demand dynamics influence the market, with alternative fuels like renewable fuels, fuel cell vehicles, and battery electric vehicles emerging as potential competitors. The industry involves fuel oil refineries, production, distribution through pipelines and tankers, and supply from various fuel oil suppliers.

The global oil and gas refining and marketing industry encompasses businesses involved in the refining and distribution of crude oil, natural gas, heavy fuel oil, marine gasoil, liquefied natural gas, liquefied petroleum gas, fuel oil blending, and fuel additives. This sector represents a significant portion of the oil and gas value chain. According to Technavio's market analysis, the expansion of this market is attributed to the escalating demand for cleaner fuels due to population growth and industrialization in emerging economies like China and India. Additionally, advancements in fuel stabilization technologies and the integration of fuel additives to enhance fuel efficiency and reduce emissions are expected to bolster market growth. Companies in this industry generate revenue through the production and sale of refined petroleum products and related services.. Industries are leveraging the products belonging to the market for customer engagement, transactional notifications, and promotional offers.

Technavio Research

Jesse Maida

Media & Marketing Executive

US: +1 844 364 1100

UK: +44 203 893 3200

Email: media@technavio.com

Website: www.technavio.com/

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.