The Air Pollution Control Market is being driven by Growing industrial development

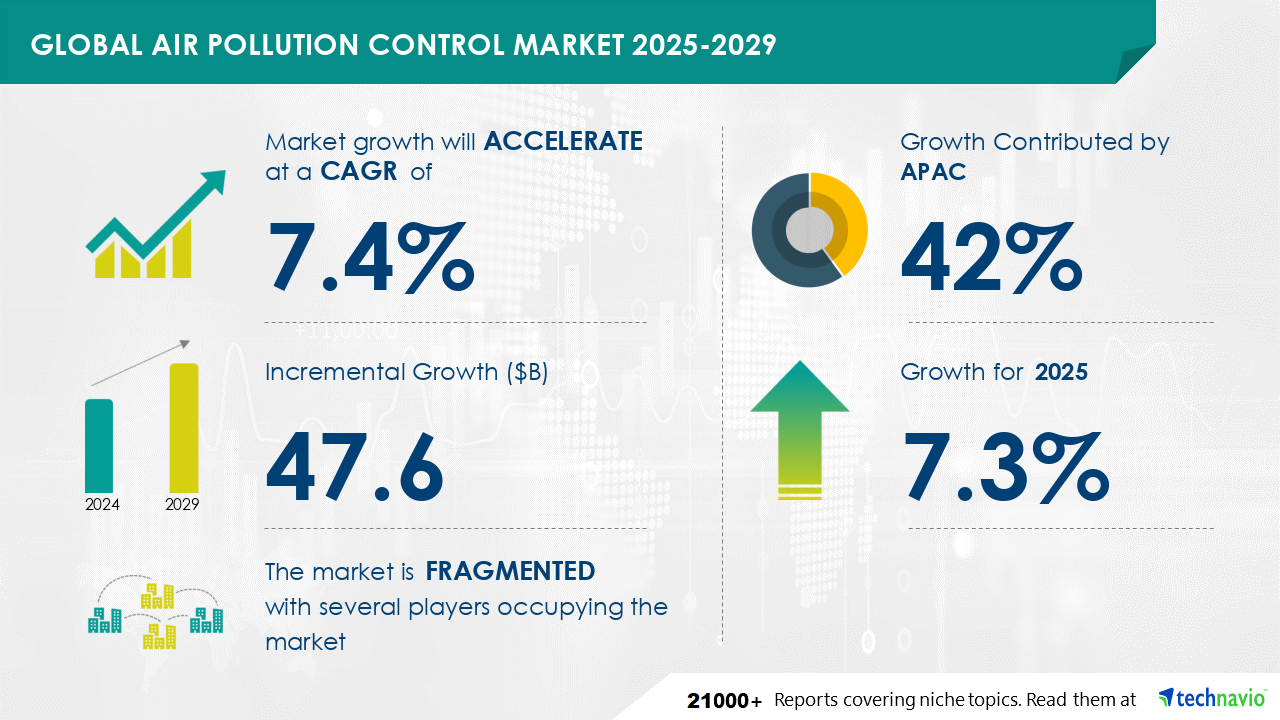

The Air Pollution Control Market is expected to grow at a CAGR of 7.4% during 2024 and 2029. During this period, the market is also expected to show a growth of USD 47.6 billion. In the realm of Air Pollution Control, Flue Gas Desulfurization (FGD) gypsum emerges as a valuable byproduct derived from FGD systems. Wet scrubber technology, integral to FGD processes, employs lime reagents or limestone for sulfur oxidation, culminating in the generation of FGD gypsum. This synthetic gypsum offers versatile applications, including agriculture, construction, mining, and water treatment. In agricultural fields, FGD gypsum is meticulously applied to soil, supplying essential nutrients such as calcium and sulfur to crops. Additionally, it promotes clay flocculation and soil aggregation, mitigating surface crusting and enhancing water infiltration. Within the construction industry, FGD gypsum finds extensive use in the production of plaster and card gypsum, employed for interior work and partitioning walls. The adoption of FGD gypsum in these applications not only contributes to environmental sustainability but also offers improved performance and durability.

Get more information on Air Pollution Control Market by requesting a sample report

The market is segmented based on

According to Technavio, There are several factors that are causing the market to flourish during the forecast period, which are as follows:

However, the market also witnesses some limitations, which are as follows:

Rich Experience: 20+ years leading global market research, trusted insights across industries.

Unlock Business Potential with Technavio: Maximize ROI with Technavio's tailored market research: deep dives and actionable insights.

Your Guide to Market Success: Empower your business with Technavio's market research and future-proof your decisions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

210 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.4% |

|

Market growth 2025-2029 |

USD 47.6 billion |

|

Market structure |

fragmentation |

|

YoY growth 2024-2025(%) |

7.3 |

|

Key countries |

China, US, Japan, Canada, Germany, South Korea, UK, Australia, India, Mexico, UAE, Brazil, China, US, Japan, Canada, Germany, South Korea, UK, Australia, India, and Mexico |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Find out which segment is leading the market by accessing the free PDF report

The Air Pollution Control Market encompasses various technologies and regulations for mitigating Stack Emissions and Fugitive Emissions. Source Reduction and End-of-pipe Control methods include Efficient Electrostatic Precipitators, Fabric Filters, Scrubber Systems, and Catalytic Converters. Regenerative Technologies like Activated Carbon and Sulfur Dioxide, Nitrogen Oxide, and Mercury Removal systems are also utilized. VOC Oxidation, Thermal Oxidation, and Wet/Dry Scrubbing are additional techniques. Air Quality Regulations, Environmental Permitting, and Compliance Monitoring are crucial. Pollution Control Software, Air Quality Modeling, and Environmental Risk Assessment aid in sustainable practices like Green Building Standards, Sustainable Development, Corporate Social Responsibility, and Environmental Sustainability. The Clean Air Act and Regulations guide Environmental Engineering and Consulting, Emissions Trading, Carbon Offsetting, and Compliance Software usage.

The global environmental and facilities services market encompasses businesses offering solutions for Air Quality Control, Emissions Reduction, Particulate Matter Control, Flue Gas Desulfurization, Nitrogen Oxide Reduction, and Mercury Control, among others. According to Technavio, market size is determined by the consolidated revenue of companies specializing in environmental and facilities maintenance services, which includes waste management, facilities management, and pollution control. Key growth drivers include the increasing prioritization of sustainability and environmental stewardship.. Industries are leveraging the products belonging to the market for customer engagement, transactional notifications, and promotional offers.

Technavio Research

Jesse Maida

Media & Marketing Executive

US: +1 844 364 1100

UK: +44 203 893 3200

Email: media@technavio.com

Website: www.technavio.com/

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.