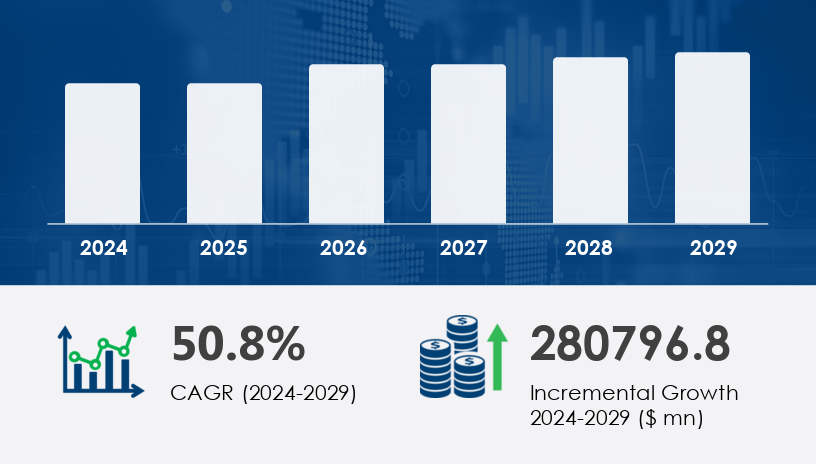

The 3D printer market is poised for extraordinary expansion, driven by rising demand across industrial and consumer sectors. In 2024, the market is estimated at a significant baseline, with forecasts predicting a surge of USD 280.8 billion by 2029, growing at a compound annual growth rate (CAGR) of 50.8%. This surge underscores the transformative impact of additive manufacturing across various industries.

For more details about the industry, get the PDF sample report for free

One of the most powerful drivers behind the 3D printer market's growth is the rising consumer interest in customized products. Additive manufacturing technology allows for personalized and complex geometries that traditional methods struggle to produce. Sectors such as automotive, aerospace, and healthcare are actively shifting towards 3D printing to streamline prototyping, reduce production costs, and enable mass customization. For instance, medical devices and prosthetics can now be tailored to individual patients, enhancing both functionality and comfort. This capability, combined with rapid prototyping, durability, and efficiency, is transforming how industries design and manufacture goods.

The increasing demand for advanced printing materials is a prominent trend reshaping the 3D printer market. Industries are actively exploring materials such as ceramics, composites, and metals to meet the growing need for durability, high precision, and thermal resistance. For example, aerospace applications require lightweight yet robust components, while healthcare demands biocompatible and sterilizable materials for implants and surgical tools. This shift towards new material development is expanding the scope of additive manufacturing beyond prototyping into full-scale production, especially in high-performance and critical-use sectors.

The 3D printer market continues to expand due to advancements in technologies such as selective laser, stereolithography, and powder bed fusion, offering versatile solutions for various applications. Techniques like vat photopolymerization, material extrusion, and direct metal printing support the creation of customized products and enhance rapid prototyping capabilities. The rise of polymer printers, metal printers, and ceramic printers addresses a growing demand for diverse material use, while desktop printers and industrial printers serve different ends of the market. Furthermore, electron beam, digital light, and binder jetting methods contribute to the growing portfolio of additive technologies used in both consumer and industrial settings.

The 3D printer market is segmented by:

Product

Industrial 3D printer

Desktop 3D printer

Technology

Fused Deposition Modeling (FDM)

Selective Laser Sintering (SLS)

Stereolithography (SLA)

Others

Material

Polymer

Metal and Ceramic

The industrial 3D printer segment dominates the market and is projected to see significant growth through 2029. Valued at USD 15.65 billion in 2019, this segment has steadily expanded as industries like aerospace, automotive, and healthcare integrate 3D printing for complex, high-precision parts. These machines are used to produce components such as jet engine parts, valves, and prosthetics, which are traditionally difficult to manufacture. According to analysts, industrial 3D printers are favored due to their ability to deliver cost-efficient, rapid prototyping and production, especially in applications requiring intricate detailing and durability.

Regions covered:

North America (Canada, US)

Europe (Germany, UK, France, Italy)

APAC (China, Japan, South Korea)

South America

Middle East and Africa

Europe is anticipated to contribute 42% to the global 3D printer market growth from 2025 to 2029, making it the leading region. The continent’s leadership is driven by strong demand in automotive, aerospace, and healthcare industries. Additionally, increased adoption of additive manufacturing in industrial sectors, coupled with support for research and development initiatives, has bolstered regional growth. Analysts note that Europe’s established infrastructure and expertise in engineering and design enable quicker adoption and scaling of 3D printing technologies, reinforcing its market leadership.

See What’s Inside: Access a Free Sample of Our In-Depth Market Research Report

Despite rapid growth, the high cost of workforce training presents a significant challenge for the 3D printer market. As this technology requires specialized knowledge in machine operation, software design, and materials science, companies often struggle to recruit and train qualified personnel. This gap can delay implementation and raise operational costs, particularly in regions or industries where technical education on 3D printing is still limited. Analysts suggest that this barrier could slow adoption rates unless addressed through targeted workforce development programs and accessible training solutions.

In-depth market studies show increasing use of 3D scanners, design software, and scanning software to streamline the pre-production phase. The importance of printer software integration is rising as manufacturers look to ensure material compatibility and enable multi-material printing for more sophisticated outputs. Demand for high-performance polymers, metal powders, and biodegradable polymers is driving material innovation, while composite materials offer enhanced durability. Growing investments in large-scale printers, precision printing, and automated post-processing reflect the trend toward smart manufacturing. Additionally, the need for functional parts and low-volume production is encouraging businesses to adopt 3D printing for more than just prototyping.

Emerging research focuses on the increasing role of 3D printing in sustainable manufacturing, particularly in sectors that require medical implants, print-on-demand solutions, and part replacement capabilities. 3D models now serve as the backbone of digital workflows, enabling faster iteration and design accuracy. Additive manufacturing supports not only prototyping tools but also full-scale production, enabled by advances in high-speed printing and consistent quality control. As the industry matures, digital workflows are being optimized to minimize waste and reduce production times. Ultimately, the integration of these technologies is shaping the future of 3D printing into a streamlined, efficient, and eco-conscious production ecosystem.

Market players are actively pursuing strategic alliances, mergers, acquisitions, and product innovations to strengthen their positions. For example, 3D Systems Corp. offers a range of advanced printers like SLA 750, DMP Factory 500, and ProX 950, addressing the needs of industries requiring high-precision metal and polymer parts.

Additionally, companies such as Desktop Metal Inc., EOS GmbH, HP Inc., and Stratasys Ltd. are pushing the boundaries of additive manufacturing through continuous R&D and expansion into new verticals like consumer electronics, fashion, and structural electronics. These firms are also investing in the development of low-cost 3D printers to broaden access and drive mass adoption.

By embracing mixed-material capabilities, standardized process controls, and advanced software integration, leading companies aim to deliver superior customization, reproducibility, and cost-efficiency. This strategic focus is instrumental in expanding market share and meeting the evolving demands of end-users.

1. Executive Summary

2. Market Landscape

3. Market Sizing

4. Historic Market Size

5. Five Forces Analysis

6. Market Segmentation

6.1 Product

6.1.1 Industrial 3D printer

6.1.2 Desktop 3D printer

6.2 Technology

6.2.1 Fused deposition modeling

6.2.2 Selective laser sintering

6.2.3 Stereolithography

6.2.4 Others

6.3 Material

6.3.1 Polymer

6.3.2 Metal and ceramic

6.4 Geography

6.4.1 North America

6.4.2 APAC

6.4.3 Europe

6.4.4 South America

6.4.5 Middle East And Africa

7. Customer Landscape

8. Geographic Landscape

9. Drivers, Challenges, and Trends

10. Company Landscape

11. Company Analysis

12. Appendix

Safe and Secure SSL Encrypted

One user only.

Quick & easy download option

Unlimited user access (Within your organization).

Complimentary Customization Included

*For Enterprise license, go to checkout page

![]() Get the report (PDF) sent to your email within minutes.

Get the report (PDF) sent to your email within minutes.